- Hong Kong

- /

- Basic Materials

- /

- SEHK:743

Asia Cement (China) Holdings' (HKG:743) Shareholders Will Receive A Bigger Dividend Than Last Year

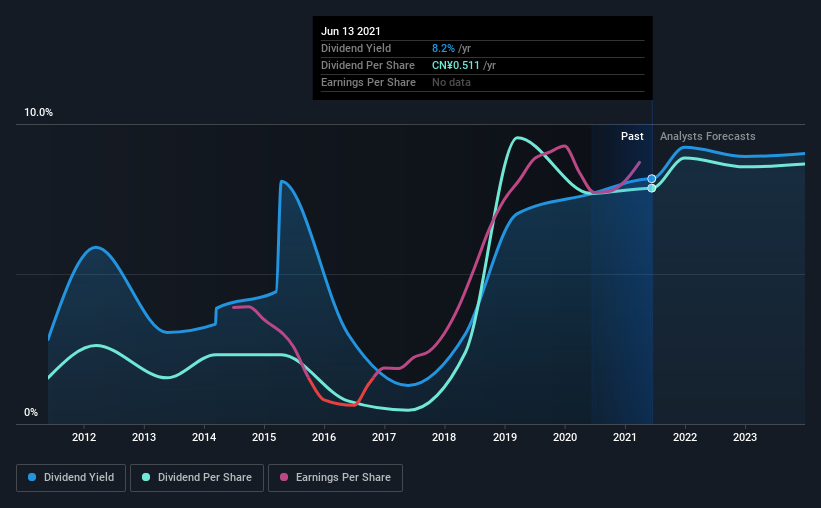

Asia Cement (China) Holdings Corporation (HKG:743) has announced that it will be increasing its dividend on the 25th of June to HK$0.62. This makes the dividend yield 8.2%, which is above the industry average.

View our latest analysis for Asia Cement (China) Holdings

Asia Cement (China) Holdings' Earnings Easily Cover the Distributions

A big dividend yield for a few years doesn't mean much if it can't be sustained. However, Asia Cement (China) Holdings' earnings easily cover the dividend. This means that most of its earnings are being retained to grow the business.

Looking forward, earnings per share is forecast to rise by 2.0% over the next year. If the dividend continues on this path, the payout ratio could be 43% by next year, which we think can be pretty sustainable going forward.

Dividend Volatility

The company's dividend history has been marked by instability, with at least 1 cut in the last 10 years. The dividend has gone from CN¥0.10 in 2011 to the most recent annual payment of CN¥0.51. This means that it has been growing its distributions at 18% per annum over that time. Dividends have grown rapidly over this time, but with cuts in the past we are not certain that this stock will be a reliable source of income in the future.

The Dividend Looks Likely To Grow

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. We are encouraged to see that Asia Cement (China) Holdings has grown earnings per share at 44% per year over the past three years. A low payout ratio gives the company a lot of flexibility, and growing earnings also make it very easy for it to grow the dividend.

We Really Like Asia Cement (China) Holdings' Dividend

In summary, it is always positive to see the dividend being increased, and we are particularly pleased with its overall sustainability. Earnings are easily covering distributions, and the company is generating plenty of cash. Taking this all into consideration, this looks like it could be a good dividend opportunity.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. As an example, we've identified 1 warning sign for Asia Cement (China) Holdings that you should be aware of before investing. If you are a dividend investor, you might also want to look at our curated list of high performing dividend stock.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:743

Asia Cement (China) Holdings

An investment holding company, manufactures and sells cement, concrete, and related products in People’s Republic of China.

Flawless balance sheet and good value.