- Hong Kong

- /

- Paper and Forestry Products

- /

- SEHK:2689

Nine Dragons Paper (Holdings)'s (HKG:2689) earnings have declined over three years, contributing to shareholders 61% loss

Nine Dragons Paper (Holdings) Limited (HKG:2689) shareholders should be happy to see the share price up 16% in the last week. But that is small recompense for the exasperating returns over three years. In that time, the share price dropped 64%. Some might say the recent bounce is to be expected after such a bad drop. The rise has some hopeful, but turnarounds are often precarious.

The recent uptick of 16% could be a positive sign of things to come, so let's take a look at historical fundamentals.

Check out our latest analysis for Nine Dragons Paper (Holdings)

In his essay The Superinvestors of Graham-and-Doddsville Warren Buffett described how share prices do not always rationally reflect the value of a business. One imperfect but simple way to consider how the market perception of a company has shifted is to compare the change in the earnings per share (EPS) with the share price movement.

During five years of share price growth, Nine Dragons Paper (Holdings) moved from a loss to profitability. We would usually expect to see the share price rise as a result. So given the share price is down it's worth checking some other metrics too.

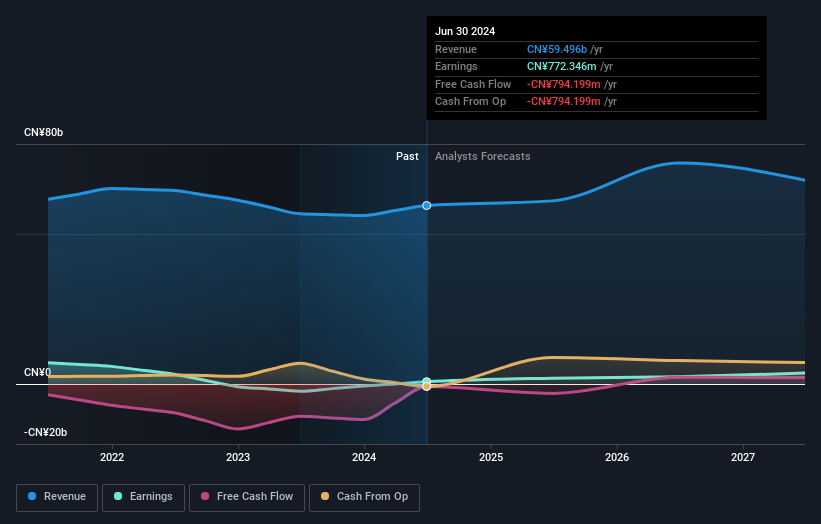

Arguably the revenue decline of 4.4% per year has people thinking Nine Dragons Paper (Holdings) is shrinking. After all, if revenue keeps shrinking, it may be difficult to find earnings growth in the future.

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

We know that Nine Dragons Paper (Holdings) has improved its bottom line lately, but what does the future have in store? This free report showing analyst forecasts should help you form a view on Nine Dragons Paper (Holdings)

What About The Total Shareholder Return (TSR)?

We've already covered Nine Dragons Paper (Holdings)'s share price action, but we should also mention its total shareholder return (TSR). The TSR attempts to capture the value of dividends (as if they were reinvested) as well as any spin-offs or discounted capital raisings offered to shareholders. Its history of dividend payouts mean that Nine Dragons Paper (Holdings)'s TSR, which was a 61% drop over the last 3 years, was not as bad as the share price return.

A Different Perspective

Nine Dragons Paper (Holdings) shareholders are down 20% for the year, but the market itself is up 14%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. Regrettably, last year's performance caps off a bad run, with the shareholders facing a total loss of 7% per year over five years. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Even so, be aware that Nine Dragons Paper (Holdings) is showing 1 warning sign in our investment analysis , you should know about...

If you are like me, then you will not want to miss this free list of undervalued small caps that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Hong Kong exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Nine Dragons Paper (Holdings) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2689

Nine Dragons Paper (Holdings)

Manufactures and sells packaging paper, printing and writing paper, and specialty paper products and pulp in the People’s Republic of China.

Reasonable growth potential and slightly overvalued.