Advertisement

- Hong Kong

- /

- Metals and Mining

- /

- SEHK:2600

Evaluating Chalco (SEHK:2600)’s Valuation After Planned Restricted Share Repurchase Review

Simply Wall St

Reviewed by Simply Wall St

Aluminum Corporation of China (SEHK:2600) has called a late November board meeting to review the repurchase and cancellation of certain unvested restricted shares, as well as an adjustment to the repurchase price.

See our latest analysis for Aluminum Corporation of China.

The upcoming decision on restricted share repurchases lands after a powerful run, with a roughly 71 percent 3 month share price return and a 3 year total shareholder return above 260 percent, suggesting momentum is still firmly building.

If this kind of corporate clean up has you thinking about positioning for the next leg of the cycle, it could be worth exploring fast growing stocks with high insider ownership.

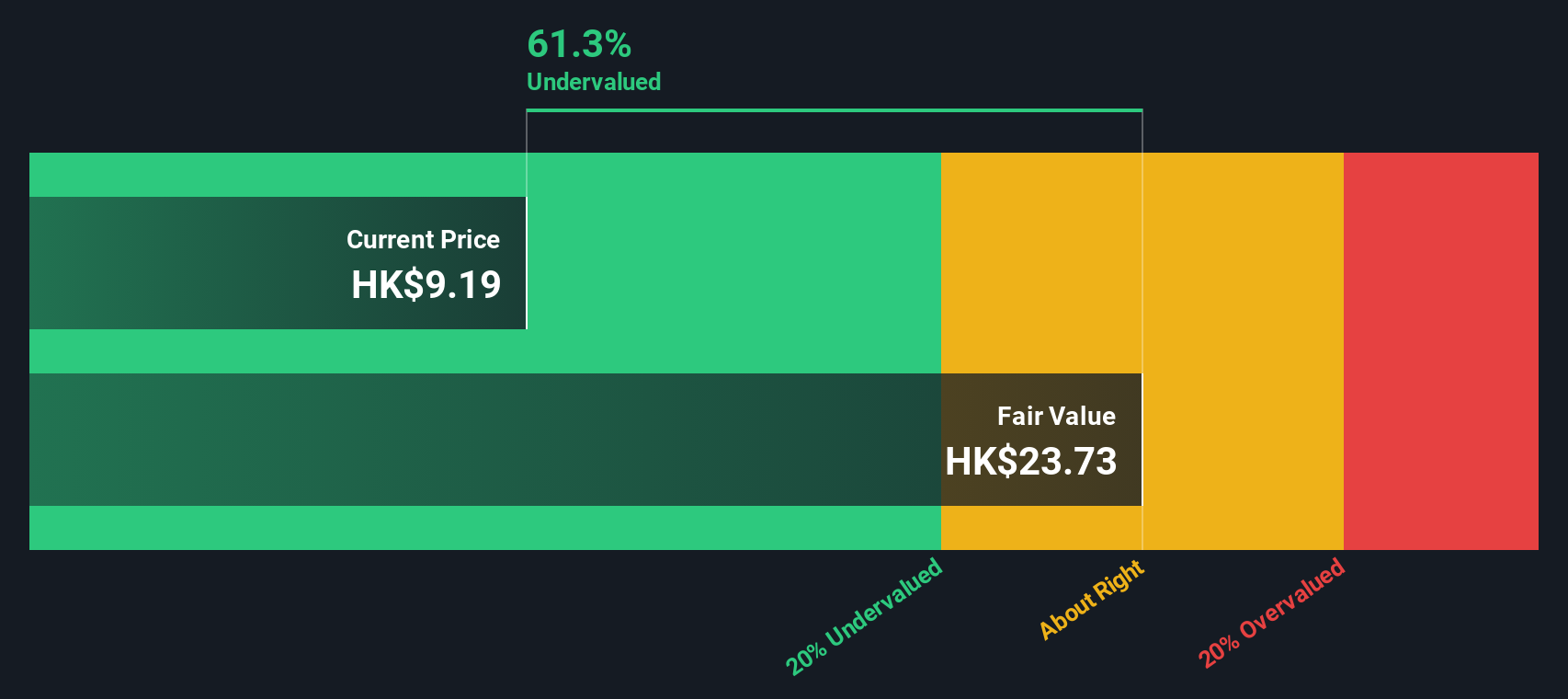

With the stock up sharply yet still trading at a hefty intrinsic discount and only a modest gap to analyst targets, investors face a key question: Is Aluminum Corporation of China still undervalued, or is future growth already priced in?

Price-to-Earnings of 12.3x: Is it justified?

Aluminum Corporation of China looks inexpensive on earnings, with a 12.3x price to earnings ratio at HK$11.21 that screens as undervalued versus both peers and the broader metals and mining space.

The price to earnings multiple compares what investors pay today to the company’s current earnings, a crucial yardstick in a cyclical, capital intensive sector like metals and mining. For Aluminum Corporation of China, solid double digit earnings growth and improving profit margins suggest the market may not be fully pricing in the company’s stronger profit base.

Relative value adds to that case. The current 12.3x price to earnings ratio sits well below the Hong Kong metals and mining industry average of 16.1x, and even further below the peer group’s 24x average, implying investors are assigning a noticeable discount despite high quality earnings and accelerated profit growth. With an estimated fair price to earnings ratio of 16.3x, the market could plausibly move toward a meaningfully higher multiple if profitability and growth trends hold.

Explore the SWS fair ratio for Aluminum Corporation of China

Result: Price-to-Earnings of 12.3x (UNDERVALUED)

However, persistent commodity price volatility and potential policy shifts in China could quickly compress margins and limit any further multiple expansion from this point.

Find out about the key risks to this Aluminum Corporation of China narrative.

Another View: DCF Points to Deeper Value

While earnings multiples suggest Aluminum Corporation of China is modestly undervalued, our DCF model paints a far starker picture, with fair value at around HK$25.62 versus the current HK$11.21. If cash flows are closer to right than sentiment, the market could be missing a much larger opportunity.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Aluminum Corporation of China for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 919 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Aluminum Corporation of China Narrative

If you see the numbers differently or want to test your own thesis, you can quickly build a personalized view in just minutes: Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Aluminum Corporation of China.

Looking for more investment ideas?

Before you move on, lock in your next move with fresh opportunities from the Simply Wall Street Screener so you are not relying on one story alone.

- Capture high potential mispricings by screening for companies trading below their estimated cash flow value using these 919 undervalued stocks based on cash flows.

- Ride the front edge of technological change by zeroing in on innovation driven names through these 25 AI penny stocks.

- Strengthen your income stream by focusing on reliable payers with attractive yields when you scan these 14 dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:2600

Aluminum Corporation of China

Primarily engages in the exploration and mining of bauxite, coal, and other resources in the People's Republic of China and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

36 followersusers have followed this narrative

6 commentsusers have commented on this narrative

10 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1918.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5190.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

114 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

952 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative