- Hong Kong

- /

- Basic Materials

- /

- SEHK:2233

Further Upside For West China Cement Limited (HKG:2233) Shares Could Introduce Price Risks After 82% Bounce

West China Cement Limited (HKG:2233) shareholders have had their patience rewarded with a 82% share price jump in the last month. Looking further back, the 24% rise over the last twelve months isn't too bad notwithstanding the strength over the last 30 days.

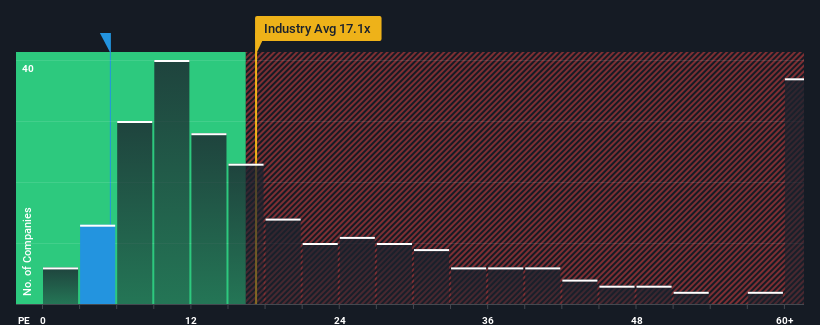

Even after such a large jump in price, given about half the companies in Hong Kong have price-to-earnings ratios (or "P/E's") above 9x, you may still consider West China Cement as an attractive investment with its 5.4x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

West China Cement has been struggling lately as its earnings have declined faster than most other companies. The P/E is probably low because investors think this poor earnings performance isn't going to improve at all. You'd much rather the company wasn't bleeding earnings if you still believe in the business. Or at the very least, you'd be hoping the earnings slide doesn't get any worse if your plan is to pick up some stock while it's out of favour.

View our latest analysis for West China Cement

Is There Any Growth For West China Cement?

The only time you'd be truly comfortable seeing a P/E as low as West China Cement's is when the company's growth is on track to lag the market.

Retrospectively, the last year delivered a frustrating 8.3% decrease to the company's bottom line. This means it has also seen a slide in earnings over the longer-term as EPS is down 38% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 52% per year during the coming three years according to the four analysts following the company. With the market only predicted to deliver 15% per year, the company is positioned for a stronger earnings result.

With this information, we find it odd that West China Cement is trading at a P/E lower than the market. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

The Final Word

The latest share price surge wasn't enough to lift West China Cement's P/E close to the market median. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Our examination of West China Cement's analyst forecasts revealed that its superior earnings outlook isn't contributing to its P/E anywhere near as much as we would have predicted. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. It appears many are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for West China Cement that you should be aware of.

If these risks are making you reconsider your opinion on West China Cement, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if West China Cement might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2233

West China Cement

An investment holding company, manufactures and sells cement and cement products in the People’s Republic of China.

High growth potential and fair value.