- Hong Kong

- /

- Metals and Mining

- /

- SEHK:1091

South Manganese Investment (HKG:1091) investors are sitting on a loss of 68% if they invested three years ago

The truth is that if you invest for long enough, you're going to end up with some losing stocks. Long term South Manganese Investment Limited (HKG:1091) shareholders know that all too well, since the share price is down considerably over three years. Regrettably, they have had to cope with a 68% drop in the share price over that period. Furthermore, it's down 27% in about a quarter. That's not much fun for holders.

Since shareholders are down over the longer term, lets look at the underlying fundamentals over the that time and see if they've been consistent with returns.

View our latest analysis for South Manganese Investment

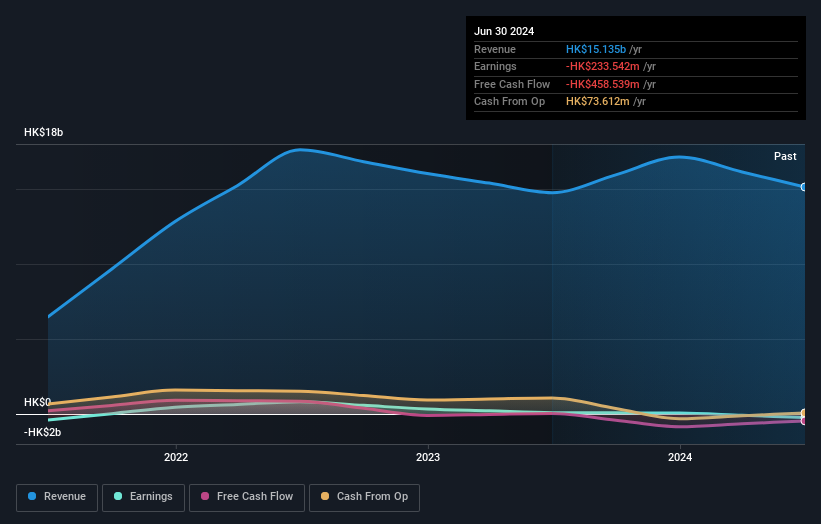

South Manganese Investment isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. Shareholders of unprofitable companies usually desire strong revenue growth. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

In the last three years, South Manganese Investment saw its revenue grow by 15% per year, compound. That's a fairly respectable growth rate. So some shareholders would be frustrated with the compound loss of 19% per year. To be frank we're surprised to see revenue growth and share price growth diverge so strongly. It would be well worth taking a closer look at the company, to determine growth trends (and balance sheet strength).

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

If you are thinking of buying or selling South Manganese Investment stock, you should check out this FREE detailed report on its balance sheet.

A Different Perspective

It's good to see that South Manganese Investment has rewarded shareholders with a total shareholder return of 61% in the last twelve months. Notably the five-year annualised TSR loss of 0.3% per year compares very unfavourably with the recent share price performance. We generally put more weight on the long term performance over the short term, but the recent improvement could hint at a (positive) inflection point within the business. You could get a better understanding of South Manganese Investment's growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

If you would prefer to check out another company -- one with potentially superior financials -- then do not miss this free list of companies that have proven they can grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Hong Kong exchanges.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1091

South Manganese Investment

An investment holding company, engages in manganese mining, ore processing, and downstream processing operations in Mainland China, Asia, Europe, and North America.

Slightly overvalued with worrying balance sheet.

Market Insights

Community Narratives