- Hong Kong

- /

- Healthcare Services

- /

- SEHK:2219

Chaoju Eye Care Holdings (HKG:2219) Is Paying Out A Larger Dividend Than Last Year

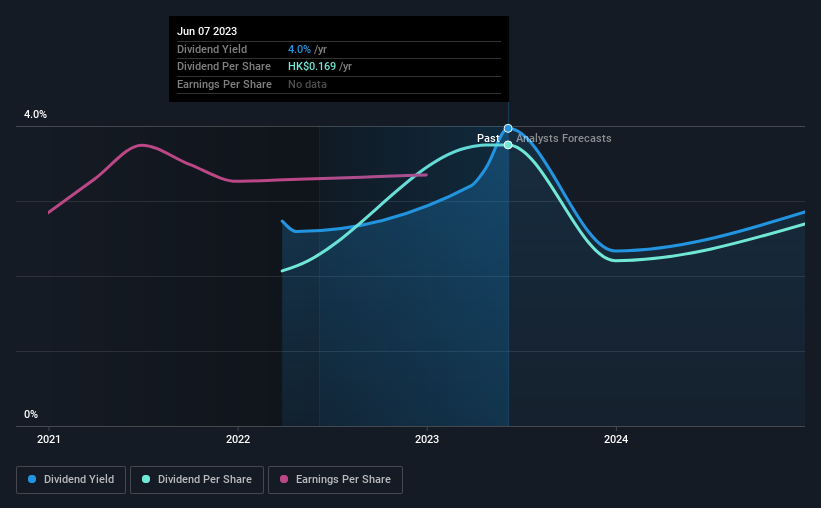

The board of Chaoju Eye Care Holdings Limited (HKG:2219) has announced that it will be paying its dividend of CN¥0.1738 on the 28th of June, an increased payment from last year's comparable dividend. This takes the dividend yield to 4.0%, which shareholders will be pleased with.

View our latest analysis for Chaoju Eye Care Holdings

Chaoju Eye Care Holdings' Payment Has Solid Earnings Coverage

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. The last dividend was quite easily covered by Chaoju Eye Care Holdings' earnings. This indicates that a lot of the earnings are being reinvested into the business, with the aim of fueling growth.

Looking forward, earnings per share is forecast to rise exponentially over the next year. Assuming the dividend continues along recent trends, we think the payout ratio will be 16%, which makes us pretty comfortable with the sustainability of the dividend.

Chaoju Eye Care Holdings Doesn't Have A Long Payment History

It's not possible for us to make a backward looking judgement just based on a short payment history. This doesn't mean that the company can't pay a good dividend, but just that we want to wait until it can prove itself.

The Dividend's Growth Prospects Are Limited

The company's investors will be pleased to have been receiving dividend income for some time. EPS hasn't moved much in the last year. That's not great, but it's also not an immediate concern - certainly better than seeing them fall. Growth of 2.6% per annum is not particularly high, which might explain why the company is paying out a higher proportion of earnings. This isn't bad in itself, but unless earnings growth pick up we wouldn't expect dividends to grow either. We do note though, one year is too short a time to be drawing strong conclusions about a company's future prospects.

Our Thoughts On Chaoju Eye Care Holdings' Dividend

Overall, it's great to see the dividend being raised and that it is still in a sustainable range. The payout ratio looks good, but unfortunately the company's dividend track record isn't stellar. Taking all of this into consideration, the dividend looks viable moving forward, but investors should be mindful that the company has pushed the boundaries of sustainability in the past and may do so again.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. For instance, we've picked out 1 warning sign for Chaoju Eye Care Holdings that investors should take into consideration. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2219

Chaoju Eye Care Holdings

Owns and operates a network of ophthalmic hospitals and optical centers in China.

Flawless balance sheet, undervalued and pays a dividend.

Market Insights

Community Narratives