Advertisement

- Hong Kong

- /

- Healthcare Services

- /

- SEHK:1846

Earnings Tell The Story For EuroEyes International Eye Clinic Limited (HKG:1846) As Its Stock Soars 27%

EuroEyes International Eye Clinic Limited (HKG:1846) shareholders would be excited to see that the share price has had a great month, posting a 27% gain and recovering from prior weakness. Unfortunately, despite the strong performance over the last month, the full year gain of 6.7% isn't as attractive.

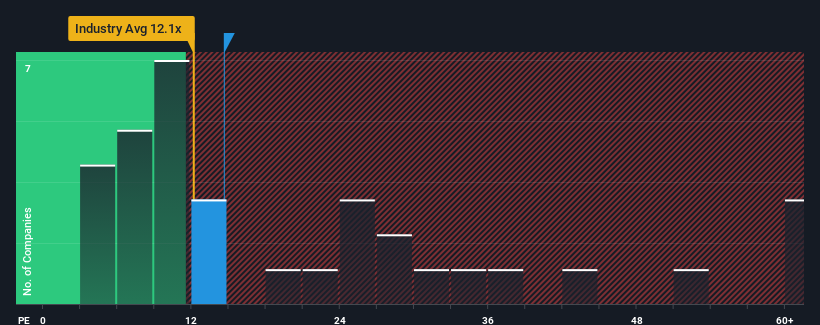

Since its price has surged higher, EuroEyes International Eye Clinic's price-to-earnings (or "P/E") ratio of 14.6x might make it look like a strong sell right now compared to the market in Hong Kong, where around half of the companies have P/E ratios below 9x and even P/E's below 5x are quite common. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

EuroEyes International Eye Clinic certainly has been doing a good job lately as it's been growing earnings more than most other companies. The P/E is probably high because investors think this strong earnings performance will continue. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for EuroEyes International Eye Clinic

Is There Enough Growth For EuroEyes International Eye Clinic?

The only time you'd be truly comfortable seeing a P/E as steep as EuroEyes International Eye Clinic's is when the company's growth is on track to outshine the market decidedly.

Taking a look back first, we see that the company grew earnings per share by an impressive 47% last year. Pleasingly, EPS has also lifted 98% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Turning to the outlook, the next year should generate growth of 52% as estimated by the dual analysts watching the company. That's shaping up to be materially higher than the 20% growth forecast for the broader market.

In light of this, it's understandable that EuroEyes International Eye Clinic's P/E sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What We Can Learn From EuroEyes International Eye Clinic's P/E?

EuroEyes International Eye Clinic's P/E is flying high just like its stock has during the last month. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of EuroEyes International Eye Clinic's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. It's hard to see the share price falling strongly in the near future under these circumstances.

Many other vital risk factors can be found on the company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for EuroEyes International Eye Clinic with six simple checks.

Of course, you might also be able to find a better stock than EuroEyes International Eye Clinic. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if EuroEyes International Eye Clinic might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1846

EuroEyes International Eye Clinic

Provides vision correction services for the treatment of myopia, presbyopia, and cataract in Germany, Denmark, the United Kingdom, and the People’s Republic of China.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor