Advertisement

- Hong Kong

- /

- Medical Equipment

- /

- SEHK:1358

Here's Why PW Medtech Group Limited's (HKG:1358) CEO Might See A Pay Rise Soon

Key Insights

- PW Medtech Group's Annual General Meeting to take place on 14th of June

- CEO Yue'e Zhang's total compensation includes salary of CN¥1.06m

- Total compensation is 59% below industry average

- PW Medtech Group's EPS declined by 38% over the past three years while total shareholder return over the past three years was 26%

Shareholders will be pleased by the robust performance of PW Medtech Group Limited (HKG:1358) recently and this will be kept in mind in the upcoming AGM on 14th of June. The focus will probably be on the future strategic initiatives that the board and management will put in place to improve the business rather than executive remuneration when they cast their votes on company resolutions. We have prepared some analysis below and we show why we think CEO compensation looks decent with even the possibility for a raise.

View our latest analysis for PW Medtech Group

Comparing PW Medtech Group Limited's CEO Compensation With The Industry

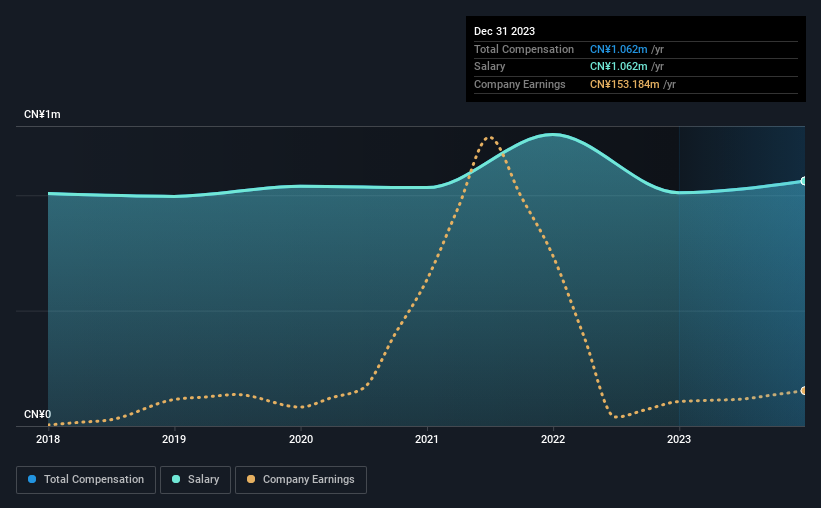

Our data indicates that PW Medtech Group Limited has a market capitalization of HK$1.7b, and total annual CEO compensation was reported as CN¥1.1m for the year to December 2023. That's just a smallish increase of 5.0% on last year. Notably, the salary of CN¥1.1m is the entirety of the CEO compensation.

On examining similar-sized companies in the Hong Kong Medical Equipment industry with market capitalizations between HK$781m and HK$3.1b, we discovered that the median CEO total compensation of that group was CN¥2.6m. This suggests that Yue'e Zhang is paid below the industry median.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | CN¥1.1m | CN¥1.0m | 100% |

| Other | - | - | - |

| Total Compensation | CN¥1.1m | CN¥1.0m | 100% |

Speaking on an industry level, nearly 64% of total compensation represents salary, while the remainder of 36% is other remuneration. On a company level, PW Medtech Group prefers to reward its CEO through a salary, opting not to pay Yue'e Zhang through non-salary benefits. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at PW Medtech Group Limited's Growth Numbers

Over the last three years, PW Medtech Group Limited has shrunk its earnings per share by 38% per year. In the last year, its revenue is up 26%.

Investors would be a bit wary of companies that have lower EPS But on the other hand, revenue growth is strong, suggesting a brighter future. These two metrics are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has PW Medtech Group Limited Been A Good Investment?

With a total shareholder return of 26% over three years, PW Medtech Group Limited shareholders would, in general, be reasonably content. But they would probably prefer not to see CEO compensation far in excess of the median.

In Summary...

PW Medtech Group pays CEO compensation exclusively through a salary, with non-salary compensation completely ignored. Overall, the company hasn't done too poorly performance-wise, but we would like to see some improvement. If it continues on the same road, shareholders might feel even more confident about their investment, and have little to no objections concerning CEO pay. In fact, strategic decisions that could impact the future of the business might be a far more interesting topic for investors as it would help them set their longer-term expectations.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. We've identified 2 warning signs for PW Medtech Group that investors should be aware of in a dynamic business environment.

Switching gears from PW Medtech Group, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1358

PW Medtech Group

An investment holding company, operates as a medical device company in China, India, the Americas, Africa, and internationally.

Excellent balance sheet and good value.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

35 followersusers have followed this narrative

6 commentsusers have commented on this narrative

10 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1918.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5190.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

113 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

952 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative