We Discuss Why Grace Wine Holdings Limited's (HKG:8146) CEO Will Find It Hard To Get A Pay Rise From Shareholders This Year

Key Insights

- Grace Wine Holdings to hold its Annual General Meeting on 5th of June

- Total pay for CEO Leissner Chan includes CN¥360.0k salary

- The overall pay is 68% below the industry average

- Grace Wine Holdings' EPS declined by 0.5% over the past three years while total shareholder loss over the past three years was 30%

The underwhelming performance at Grace Wine Holdings Limited (HKG:8146) recently has probably not pleased shareholders. The next AGM coming up on 5th of June will be a chance for shareholders to have their concerns addressed by the board, challenge management on company strategy and vote on resolutions such as executive remuneration, which may help change the company's future prospects. We think most shareholders will probably pass the CEO compensation, based on what we gathered.

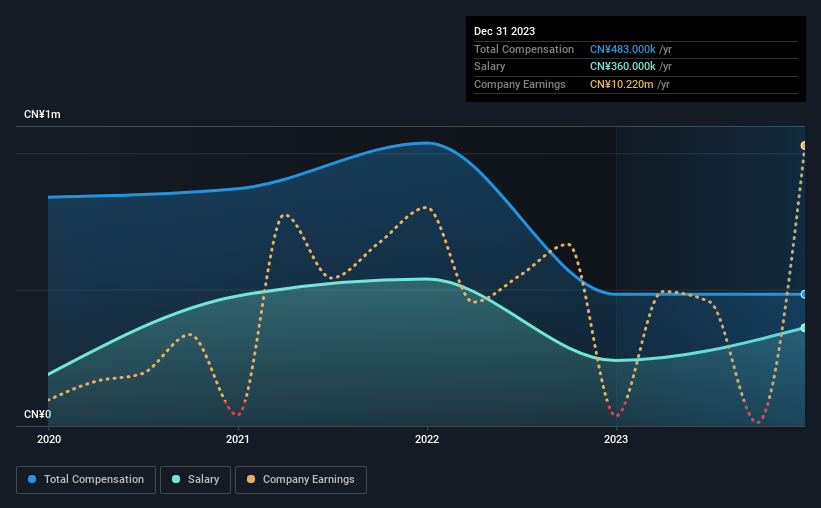

See our latest analysis for Grace Wine Holdings

Comparing Grace Wine Holdings Limited's CEO Compensation With The Industry

Our data indicates that Grace Wine Holdings Limited has a market capitalization of HK$111m, and total annual CEO compensation was reported as CN¥483k for the year to December 2023. There was no change in the compensation compared to last year. We note that the salary portion, which stands at CN¥360.0k constitutes the majority of total compensation received by the CEO.

On comparing similar-sized companies in the Hong Kong Beverage industry with market capitalizations below HK$1.6b, we found that the median total CEO compensation was CN¥1.5m. Accordingly, Grace Wine Holdings pays its CEO under the industry median. What's more, Leissner Chan holds HK$82m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | CN¥360k | CN¥240k | 75% |

| Other | CN¥123k | CN¥243k | 25% |

| Total Compensation | CN¥483k | CN¥483k | 100% |

Talking in terms of the industry, salary represented approximately 74% of total compensation out of all the companies we analyzed, while other remuneration made up 26% of the pie. Our data reveals that Grace Wine Holdings allocates salary more or less in line with the wider market. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Grace Wine Holdings Limited's Growth

Grace Wine Holdings Limited saw earnings per share stay pretty flat over the last three years. In the last year, its revenue is up 4.6%.

Its a bit disappointing to see that the company has failed to grow its EPS. And the modest revenue growth over 12 months isn't much comfort against the reduced EPS. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Grace Wine Holdings Limited Been A Good Investment?

Given the total shareholder loss of 30% over three years, many shareholders in Grace Wine Holdings Limited are probably rather dissatisfied, to say the least. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

Not only have shareholders not seen a favorable return on their investment, but the business hasn't performed well either. Few shareholders would be willing to award the CEO with a pay raise. At the upcoming AGM, management will get a chance to explain how they plan to get the business back on track and address the concerns from investors.

CEO pay is simply one of the many factors that need to be considered while examining business performance. In our study, we found 2 warning signs for Grace Wine Holdings you should be aware of, and 1 of them is concerning.

Important note: Grace Wine Holdings is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

If you're looking to trade Grace Wine Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:8146

Grace Wine Holdings

An investment holding company, engages in the production and distribution of wine, spirits, and other alcoholic products in Hong Kong, Mainland China, and internationally.

Slight with mediocre balance sheet.

Market Insights

Community Narratives