Cautious Investors Not Rewarding New Silkroad Culturaltainment Limited's (HKG:472) Performance Completely

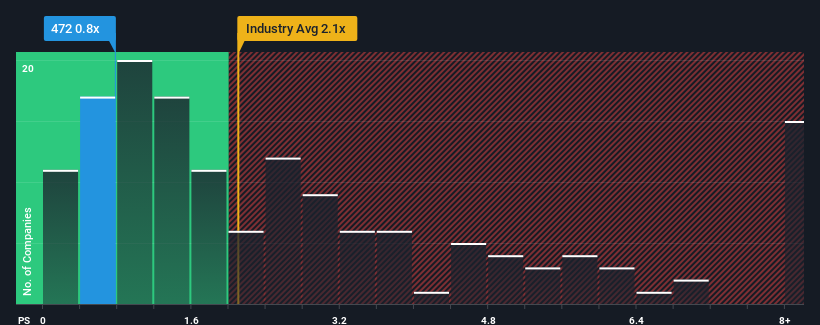

When close to half the companies operating in the Beverage industry in Hong Kong have price-to-sales ratios (or "P/S") above 1.7x, you may consider New Silkroad Culturaltainment Limited (HKG:472) as an attractive investment with its 0.8x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

See our latest analysis for New Silkroad Culturaltainment

What Does New Silkroad Culturaltainment's P/S Mean For Shareholders?

With revenue growth that's exceedingly strong of late, New Silkroad Culturaltainment has been doing very well. One possibility is that the P/S ratio is low because investors think this strong revenue growth might actually underperform the broader industry in the near future. Those who are bullish on New Silkroad Culturaltainment will be hoping that this isn't the case, so that they can pick up the stock at a lower valuation.

Although there are no analyst estimates available for New Silkroad Culturaltainment, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Do Revenue Forecasts Match The Low P/S Ratio?

The only time you'd be truly comfortable seeing a P/S as low as New Silkroad Culturaltainment's is when the company's growth is on track to lag the industry.

Retrospectively, the last year delivered an exceptional 142% gain to the company's top line. The latest three year period has also seen an incredible overall rise in revenue, aided by its incredible short-term performance. Accordingly, shareholders would have been over the moon with those medium-term rates of revenue growth.

When compared to the industry's one-year growth forecast of 9.9%, the most recent medium-term revenue trajectory is noticeably more alluring

With this in mind, we find it intriguing that New Silkroad Culturaltainment's P/S isn't as high compared to that of its industry peers. Apparently some shareholders believe the recent performance has exceeded its limits and have been accepting significantly lower selling prices.

The Final Word

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of New Silkroad Culturaltainment revealed its three-year revenue trends aren't boosting its P/S anywhere near as much as we would have predicted, given they look better than current industry expectations. When we see strong revenue with faster-than-industry growth, we assume there are some significant underlying risks to the company's ability to make money which is applying downwards pressure on the P/S ratio. At least price risks look to be very low if recent medium-term revenue trends continue, but investors seem to think future revenue could see a lot of volatility.

It is also worth noting that we have found 2 warning signs for New Silkroad Culturaltainment (1 is a bit unpleasant!) that you need to take into consideration.

If these risks are making you reconsider your opinion on New Silkroad Culturaltainment, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if New Silkroad Culturaltainment might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:472

New Silkroad Culturaltainment

An investment holding company, engages in the provision of property management services in the People’s Republic of China.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Community Narratives