Market Might Still Lack Some Conviction On China Tontine Wines Group Limited (HKG:389) Even After 40% Share Price Boost

China Tontine Wines Group Limited (HKG:389) shareholders have had their patience rewarded with a 40% share price jump in the last month. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 10% over that time.

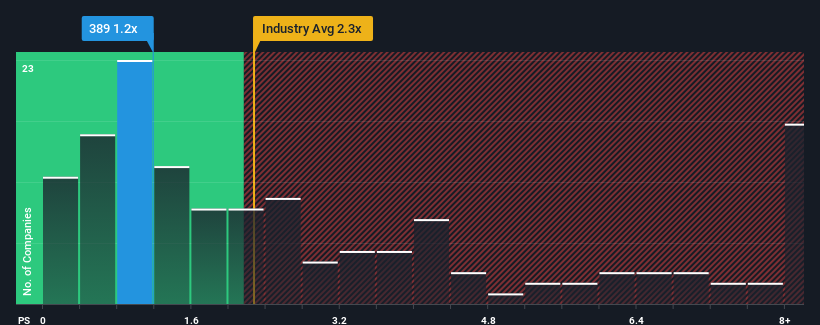

Even after such a large jump in price, you could still be forgiven for feeling indifferent about China Tontine Wines Group's P/S ratio of 1.2x, since the median price-to-sales (or "P/S") ratio for the Beverage industry in Hong Kong is also close to 1.6x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

View our latest analysis for China Tontine Wines Group

What Does China Tontine Wines Group's Recent Performance Look Like?

Revenue has risen firmly for China Tontine Wines Group recently, which is pleasing to see. One possibility is that the P/S is moderate because investors think this respectable revenue growth might not be enough to outperform the broader industry in the near future. Those who are bullish on China Tontine Wines Group will be hoping that this isn't the case, so that they can pick up the stock at a lower valuation.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on China Tontine Wines Group will help you shine a light on its historical performance.How Is China Tontine Wines Group's Revenue Growth Trending?

In order to justify its P/S ratio, China Tontine Wines Group would need to produce growth that's similar to the industry.

Retrospectively, the last year delivered an exceptional 29% gain to the company's top line. The latest three year period has also seen an excellent 75% overall rise in revenue, aided by its short-term performance. Therefore, it's fair to say the revenue growth recently has been superb for the company.

When compared to the industry's one-year growth forecast of 13%, the most recent medium-term revenue trajectory is noticeably more alluring

With this information, we find it interesting that China Tontine Wines Group is trading at a fairly similar P/S compared to the industry. Apparently some shareholders believe the recent performance is at its limits and have been accepting lower selling prices.

The Key Takeaway

China Tontine Wines Group appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We didn't quite envision China Tontine Wines Group's P/S sitting in line with the wider industry, considering the revenue growth over the last three-year is higher than the current industry outlook. There could be some unobserved threats to revenue preventing the P/S ratio from matching this positive performance. While recent revenue trends over the past medium-term suggest that the risk of a price decline is low, investors appear to see the likelihood of revenue fluctuations in the future.

We don't want to rain on the parade too much, but we did also find 3 warning signs for China Tontine Wines Group (1 is a bit unpleasant!) that you need to be mindful of.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:389

China Tontine Wines Group

An investment holding company, produces and sells grape wine in the People’s Republic of China.

Moderate and good value.

Market Insights

Community Narratives