Advertisement

Four Seas Mercantile (SEHK:374) Margins Drop to 0.08%, Undercutting Bullish Value Narratives

Simply Wall St

Reviewed by Simply Wall St

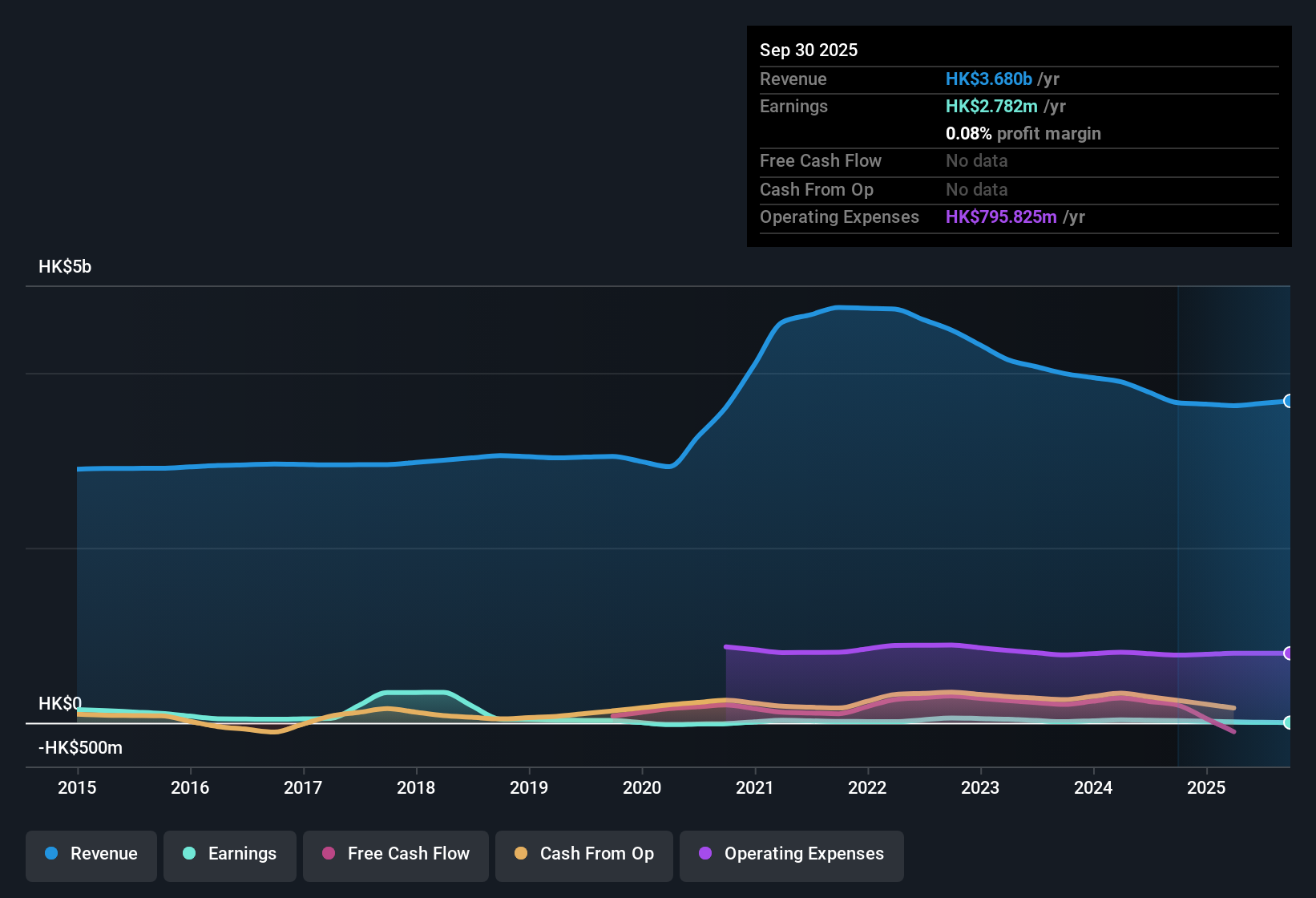

Four Seas Mercantile Holdings (SEHK:374) has just posted its H1 2026 results, reporting revenue of $1.9 billion HKD and a basic EPS of -0.027 HKD, with net income excluding extraordinary items at -10.3 million HKD. Looking back, the company has seen revenue fluctuate from $1.7 billion HKD in H1 2025 to $1.9 billion HKD in H2 2025, while basic EPS shifted from 0.053 HKD to -0.027 HKD over the same periods. Margins remained under pressure this half, leaving investors evaluating the impact on future profitability.

See our full analysis for Four Seas Mercantile Holdings.Next up, we will see how these latest numbers compare to the community narratives that have shaped expectations around Four Seas Mercantile Holdings. This will set the stage for a reality check and fresh perspectives.

Curious how numbers become stories that shape markets? Explore Community Narratives

Profit Margins Hit New Low at 0.08%

- Trailing twelve month net profit margins have dropped to 0.08%, down from 0.7% last year. Net income for H1 2026 stands at $2.8 million HKD on $3.7 billion HKD in revenue.

- Bears highlight that persistently low margins present a stark contrast to the company’s previous years and raise concerns about the sustainability of profitability, especially as interest payments remain insufficiently covered by current earnings.

- This risk appears particularly pressing given that five-year average earnings growth is -0.8%, with no recent sign of improvement.

- Even with small TTM profits, the inability to consistently outpace costs could further strain already thin margins.

Share Price Lags Estimated Fair Value

- At a current share price of 2.68 HKD, Four Seas Mercantile Holdings trades 15.2% below its estimated DCF fair value of 3.16 HKD. This suggests potential value support.

- Market opinion notes that the low 0.3x price-to-sales ratio, compared to the Hong Kong food industry average of 0.7x, could make the stock appealing for value-focused investors provided margin pressures do not worsen.

- Despite the discount, ongoing profitability and dividend coverage issues may leave some investors cautious and could limit immediate upside.

- If management succeeds in stabilizing or improving profitability, valuation multiples could move closer to sector norms.

Dividend Yield Undercut by Weak Coverage

- The trailing twelve month dividend yield stands at 3.54%, but analysis finds current earnings and free cash flow do not adequately support this payout.

- According to prevailing analysis, the risk of an unsustainable dividend adds to existing financial challenges as coverage ratios fall short and past earnings contraction continues to have an impact.

- Dividend payouts could be at risk unless profitability and cash generation improve in future periods.

- The low margin environment means investors relying on income face heightened volatility tied to core financial health.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Four Seas Mercantile Holdings's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

With shrinking profit margins, weak dividend coverage, and ongoing earnings pressures, Four Seas Mercantile Holdings is struggling to demonstrate reliable financial health and income stability.

If sustained payouts and resilience matter to you, check out these 1922 dividend stocks with yields > 3% to discover companies with stronger yields and more dependable financial coverage.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:374

Four Seas Mercantile Holdings

An investment holding company, engages in the manufacture and trade in snack food, confectionery, beverages, frozen food products, noodles, and ham and ham-related products in Hong Kong, Mainland China, and Japan.

Fair value with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

139 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

931 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative