Advertisement

- Hong Kong

- /

- Oil and Gas

- /

- SEHK:883

CNOOC Limited Just Beat Revenue By 5.4%: Here's What Analysts Think Will Happen Next

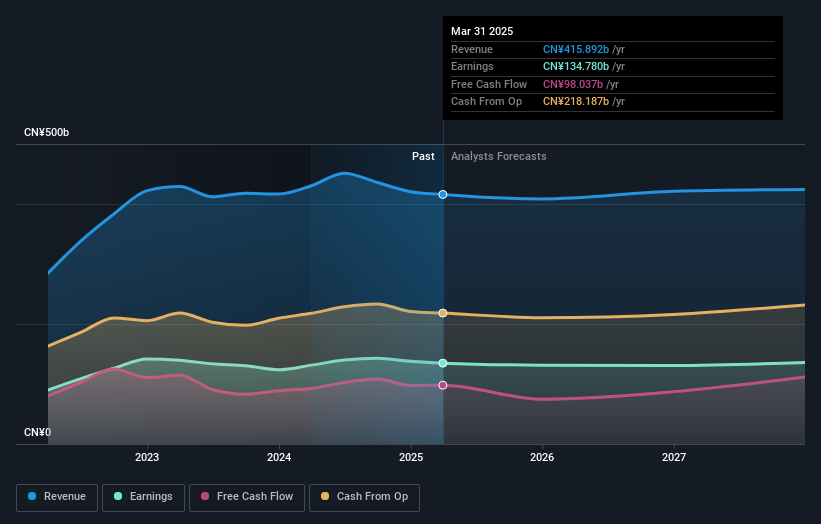

Last week saw the newest first-quarter earnings release from CNOOC Limited (HKG:883), an important milestone in the company's journey to build a stronger business. Results overall were respectable, with statutory earnings of CN¥0.77 per share roughly in line with what the analysts had forecast. Revenues of CN¥107b came in 5.4% ahead of analyst predictions. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on CNOOC after the latest results.

Taking into account the latest results, CNOOC's 15 analysts currently expect revenues in 2025 to be CN¥408.4b, approximately in line with the last 12 months. Statutory per share are forecast to be CN¥2.80, approximately in line with the last 12 months. In the lead-up to this report, the analysts had been modelling revenues of CN¥420.2b and earnings per share (EPS) of CN¥2.88 in 2025. The analysts are less bullish than they were before these results, given the reduced revenue forecasts and the small dip in earnings per share expectations.

View our latest analysis for CNOOC

The analysts made no major changes to their price target of HK$21.07, suggesting the downgrades are not expected to have a long-term impact on CNOOC's valuation. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. The most optimistic CNOOC analyst has a price target of HK$27.39 per share, while the most pessimistic values it at HK$10.55. This is a fairly broad spread of estimates, suggesting that analysts are forecasting a wide range of possible outcomes for the business.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. These estimates imply that revenue is expected to slow, with a forecast annualised decline of 2.4% by the end of 2025. This indicates a significant reduction from annual growth of 20% over the last five years. Yet aggregate analyst estimates for other companies in the industry suggest that industry revenues are forecast to decline 0.4% per year. So it's pretty clear that CNOOC's revenues are expected to shrink faster than the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for CNOOC. Unfortunately they also downgraded their revenue estimates, and our analysts estimates suggest that CNOOC is still expected to perform worse than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have forecasts for CNOOC going out to 2027, and you can see them free on our platform here.

Don't forget that there may still be risks. For instance, we've identified 2 warning signs for CNOOC (1 is a bit concerning) you should be aware of.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:883

CNOOC

An investment holding company, engages in the exploration, development, production, and sale of crude oil and natural gas in the People’s Republic of China, Canada, and internationally.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor