- Hong Kong

- /

- Oil and Gas

- /

- SEHK:702

Can Sino Oil and Gas Holdings (HKG:702) Continue To Grow Its Returns On Capital?

If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. With that in mind, we've noticed some promising trends at Sino Oil and Gas Holdings (HKG:702) so let's look a bit deeper.

What is Return On Capital Employed (ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. Analysts use this formula to calculate it for Sino Oil and Gas Holdings:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

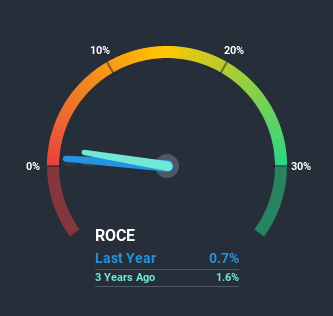

0.0068 = HK$22m ÷ (HK$5.0b - HK$1.7b) (Based on the trailing twelve months to June 2020).

So, Sino Oil and Gas Holdings has an ROCE of 0.7%. Ultimately, that's a low return and it under-performs the Oil and Gas industry average of 6.8%.

View our latest analysis for Sino Oil and Gas Holdings

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating Sino Oil and Gas Holdings' past further, check out this free graph of past earnings, revenue and cash flow.

What The Trend Of ROCE Can Tell Us

It's nice to see that ROCE is headed in the right direction, even if it is still relatively low. The figures show that over the last five years, returns on capital have grown by 177%. The company is now earning HK$0.007 per dollar of capital employed. Interestingly, the business may be becoming more efficient because it's applying 28% less capital than it was five years ago. Sino Oil and Gas Holdings may be selling some assets so it's worth investigating if the business has plans for future investments to increase returns further still.

On a side note, we noticed that the improvement in ROCE appears to be partly fueled by an increase in current liabilities. Effectively this means that suppliers or short-term creditors are now funding 34% of the business, which is more than it was five years ago. It's worth keeping an eye on this because as the percentage of current liabilities to total assets increases, some aspects of risk also increase.

The Bottom Line

In summary, it's great to see that Sino Oil and Gas Holdings has been able to turn things around and earn higher returns on lower amounts of capital. Although the company may be facing some issues elsewhere since the stock has plunged 84% in the last five years. Still, it's worth doing some further research to see if the trends will continue into the future.

Sino Oil and Gas Holdings does come with some risks though, we found 2 warning signs in our investment analysis, and 1 of those can't be ignored...

While Sino Oil and Gas Holdings may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

When trading Sino Oil and Gas Holdings or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:702

Sino Oil and Gas Holdings

An investment holding company, engages in exploration, development, and production of coalbed methane in Hong Kong and the People's Republic of China.

Good value slight.

Similar Companies

Market Insights

Community Narratives