Advertisement

- Hong Kong

- /

- Oil and Gas

- /

- SEHK:689

EPI (Holdings) Limited (HKG:689) Stocks Shoot Up 30% But Its P/S Still Looks Reasonable

EPI (Holdings) Limited (HKG:689) shares have continued their recent momentum with a 30% gain in the last month alone. The bad news is that even after the stocks recovery in the last 30 days, shareholders are still underwater by about 9.1% over the last year.

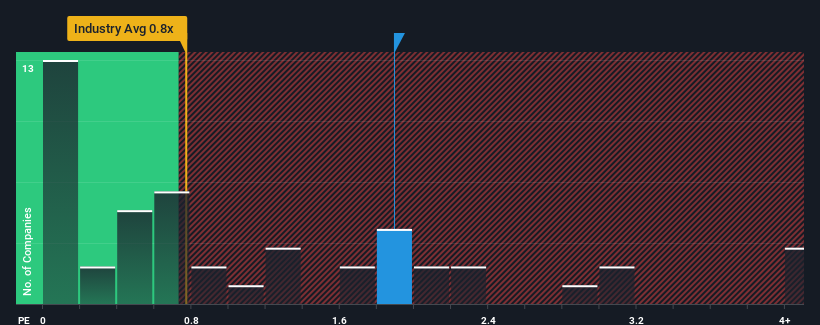

Since its price has surged higher, given close to half the companies operating in Hong Kong's Oil and Gas industry have price-to-sales ratios (or "P/S") below 0.8x, you may consider EPI (Holdings) as a stock to potentially avoid with its 1.9x P/S ratio. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for EPI (Holdings)

What Does EPI (Holdings)'s P/S Mean For Shareholders?

With revenue growth that's exceedingly strong of late, EPI (Holdings) has been doing very well. It seems that many are expecting the strong revenue performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. However, if this isn't the case, investors might get caught out paying too much for the stock.

Although there are no analyst estimates available for EPI (Holdings), take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Is There Enough Revenue Growth Forecasted For EPI (Holdings)?

The only time you'd be truly comfortable seeing a P/S as high as EPI (Holdings)'s is when the company's growth is on track to outshine the industry.

Retrospectively, the last year delivered an exceptional 84% gain to the company's top line. The latest three year period has also seen an excellent 96% overall rise in revenue, aided by its short-term performance. Therefore, it's fair to say the revenue growth recently has been superb for the company.

When compared to the industry's one-year growth forecast of 1.7%, the most recent medium-term revenue trajectory is noticeably more alluring

With this information, we can see why EPI (Holdings) is trading at such a high P/S compared to the industry. Presumably shareholders aren't keen to offload something they believe will continue to outmanoeuvre the wider industry.

The Key Takeaway

EPI (Holdings) shares have taken a big step in a northerly direction, but its P/S is elevated as a result. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of EPI (Holdings) revealed its three-year revenue trends are contributing to its high P/S, given they look better than current industry expectations. At this stage investors feel the potential continued revenue growth in the future is great enough to warrant an inflated P/S. Barring any significant changes to the company's ability to make money, the share price should continue to be propped up.

It is also worth noting that we have found 3 warning signs for EPI (Holdings) that you need to take into consideration.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're here to simplify it.

Discover if EPI (Holdings) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:689

EPI (Holdings)

An investment holding company, primarily engages in the exploration and production of petroleum in Canada and Hong Kong.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.3% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.0% undervalued

TI

Community Contributor