- Hong Kong

- /

- Oil and Gas

- /

- SEHK:467

Revenues Tell The Story For United Energy Group Limited (HKG:467) As Its Stock Soars 31%

The United Energy Group Limited (HKG:467) share price has done very well over the last month, posting an excellent gain of 31%. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 46% in the last twelve months.

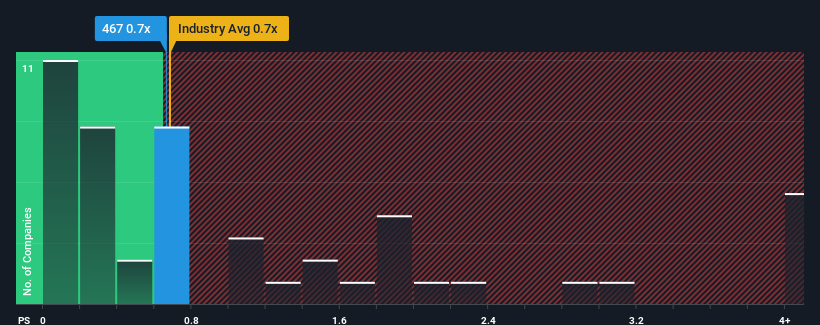

Although its price has surged higher, you could still be forgiven for feeling indifferent about United Energy Group's P/S ratio of 0.7x, since the median price-to-sales (or "P/S") ratio for the Oil and Gas industry in Hong Kong is about the same. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

See our latest analysis for United Energy Group

How Has United Energy Group Performed Recently?

With its revenue growth in positive territory compared to the declining revenue of most other companies, United Energy Group has been doing quite well of late. It might be that many expect the strong revenue performance to deteriorate like the rest, which has kept the P/S ratio from rising. If not, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on United Energy Group.How Is United Energy Group's Revenue Growth Trending?

The only time you'd be comfortable seeing a P/S like United Energy Group's is when the company's growth is tracking the industry closely.

Retrospectively, the last year delivered an exceptional 44% gain to the company's top line. The strong recent performance means it was also able to grow revenue by 133% in total over the last three years. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Turning to the outlook, the next year should generate growth of 2.4% as estimated by the two analysts watching the company. That's shaping up to be similar to the 2.0% growth forecast for the broader industry.

In light of this, it's understandable that United Energy Group's P/S sits in line with the majority of other companies. Apparently shareholders are comfortable to simply hold on while the company is keeping a low profile.

What We Can Learn From United Energy Group's P/S?

United Energy Group appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Our look at United Energy Group's revenue growth estimates show that its P/S is about what we expect, as both metrics follow closely with the industry averages. Right now shareholders are comfortable with the P/S as they are quite confident future revenue won't throw up any surprises. Unless these conditions change, they will continue to support the share price at these levels.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 1 warning sign with United Energy Group, and understanding should be part of your investment process.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

If you're looking to trade United Energy Group, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:467

United Energy Group

An investment holding company, engages in the investment and operation of upstream oil, natural gas, clean energy, and energy trading businesses in South Asia, the Middle East, and North Africa.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Community Narratives