Advertisement

As global markets navigate an era of heightened uncertainty, the Asian market continues to capture investor interest with its diverse opportunities. Penny stocks, often associated with smaller or newer companies, remain relevant as they present potential growth at lower price points. When backed by robust financials and solid fundamentals, these stocks can offer unique opportunities for investors seeking hidden gems poised for long-term success.

Top 10 Penny Stocks In Asia

| Name | Share Price | Market Cap | Rewards & Risks |

| Interlink Telecom (SET:ITEL) | THB1.41 | THB1.97B | ✅ 4 ⚠️ 5 View Analysis > |

| Beng Kuang Marine (SGX:BEZ) | SGD0.205 | SGD40.84M | ✅ 4 ⚠️ 3 View Analysis > |

| Hong Leong Asia (SGX:H22) | SGD1.21 | SGD845.33M | ✅ 4 ⚠️ 1 View Analysis > |

| Yangzijiang Shipbuilding (Holdings) (SGX:BS6) | SGD2.40 | SGD9.56B | ✅ 5 ⚠️ 0 View Analysis > |

| YesAsia Holdings (SEHK:2209) | HK$3.11 | HK$1.23B | ✅ 4 ⚠️ 4 View Analysis > |

| IGG (SEHK:799) | HK$3.83 | HK$4.9B | ✅ 5 ⚠️ 1 View Analysis > |

| Bosideng International Holdings (SEHK:3998) | HK$4.02 | HK$45.16B | ✅ 4 ⚠️ 1 View Analysis > |

| Lever Style (SEHK:1346) | HK$1.33 | HK$820.24M | ✅ 4 ⚠️ 1 View Analysis > |

| China Zheshang Bank (SEHK:2016) | HK$2.56 | HK$83.2B | ✅ 4 ⚠️ 1 View Analysis > |

| Xiamen Hexing Packaging Printing (SZSE:002228) | CN¥3.15 | CN¥3.64B | ✅ 3 ⚠️ 1 View Analysis > |

Click here to see the full list of 1,172 stocks from our Asian Penny Stocks screener.

Here we highlight a subset of our preferred stocks from the screener.

Best Mart 360 Holdings (SEHK:2360)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Best Mart 360 Holdings Limited is an investment holding company that operates as a leisure food retailer with chain retail stores under the Best Mart 360 and FoodVille brands in Hong Kong, Macau, and the People’s Republic of China, with a market cap of HK$1.74 billion.

Operations: No revenue segments are reported for Best Mart 360 Holdings Limited.

Market Cap: HK$1.74B

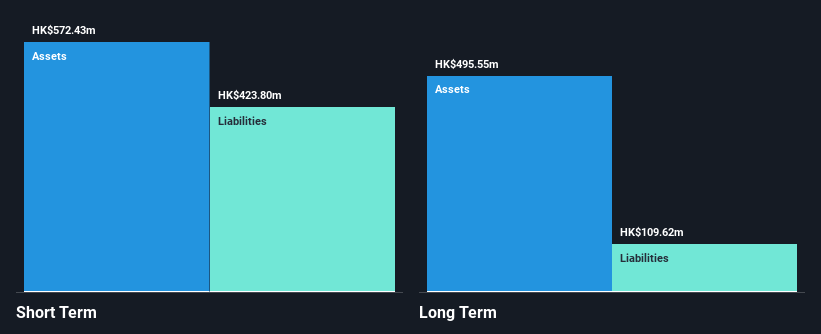

Best Mart 360 Holdings has shown a steady earnings growth of 10.3% over the past year, surpassing the Consumer Retailing industry decline of 7.2%. Despite an inexperienced board and management team, the company maintains high-quality earnings with an outstanding Return on Equity of 46.3%. Its financial health is robust, with short-term assets exceeding liabilities and debt well-covered by operating cash flow (612.9%). The company trades at a significant discount to its estimated fair value and has reduced its debt-to-equity ratio from 32.5% to 13.7% over five years, indicating strong financial management amidst stable weekly volatility (2%).

- Unlock comprehensive insights into our analysis of Best Mart 360 Holdings stock in this financial health report.

- Gain insights into Best Mart 360 Holdings' historical outcomes by reviewing our past performance report.

Anton Oilfield Services Group (SEHK:3337)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Anton Oilfield Services Group is an investment holding company that offers oilfield engineering and technical services to oil companies in China, Iraq, and internationally, with a market cap of HK$2.78 billion.

Operations: The company generates revenue from various segments including CN¥2.13 billion from Oilfield Technical Services, CN¥1.85 billion from Oilfield Management Services, CN¥421.04 million from Inspection Services, and CN¥358.89 million from Drilling Rig Services.

Market Cap: HK$2.78B

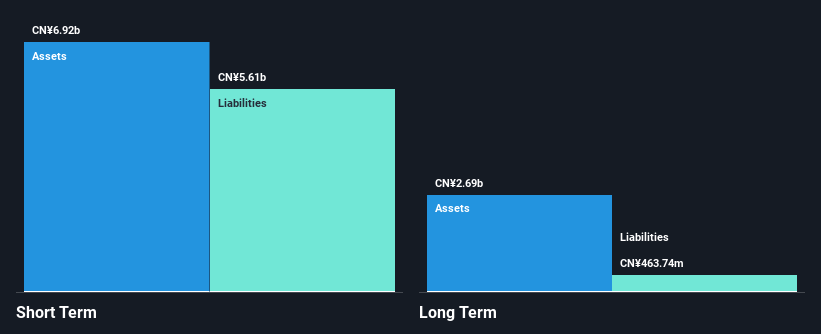

Anton Oilfield Services Group has demonstrated robust financial health, with short-term assets of CN¥7.5 billion comfortably exceeding both its long-term liabilities of CN¥470.9 million and short-term liabilities of CN¥6.1 billion. The company reported a net income increase to CN¥242.65 million for 2024, reflecting a year-on-year earnings growth of 23.5%, which outpaces the industry average and highlights strong operational performance despite low return on equity (7.1%). Debt management is commendable with a reduced debt-to-equity ratio from 166.9% to 67.6% over five years, supported by well-covered interest payments and operating cash flow coverage at 54%.

- Get an in-depth perspective on Anton Oilfield Services Group's performance by reading our balance sheet health report here.

- Gain insights into Anton Oilfield Services Group's future direction by reviewing our growth report.

Japfa (SGX:UD2)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Japfa Ltd. is an agri-food company that produces and sells protein staples and packaged food products in Indonesia, Vietnam, India, Myanmar, and internationally with a market cap of SGD1.17 billion.

Operations: The company's revenue is primarily derived from its Animal Protein - PT Japfa Tbk (Incl. Consumer Food) segment, which generated $3.51 billion, and the Animal Protein - Other segment, contributing $1.08 billion.

Market Cap: SGD1.17B

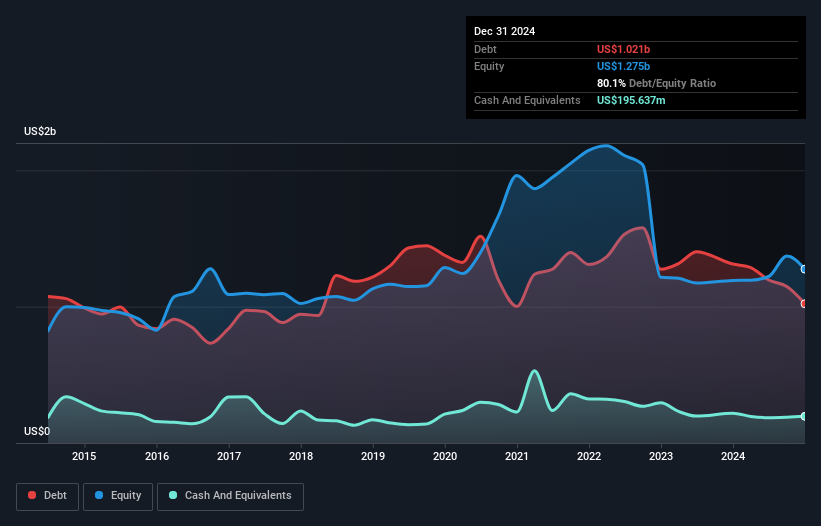

Japfa Ltd. has shown financial resilience, with short-term assets of $1.4 billion exceeding its liabilities, and a reduction in the debt-to-equity ratio from 107% to 80.1% over five years. The company became profitable last year, reporting net income of US$113.57 million for 2024 compared to a loss previously, though its return on equity remains low at 16.3%. Japfa's shares may soon be delisted following a privatization offer at SGD0.62 per share by major shareholders, representing a premium over recent trading prices and reflecting strategic shifts within the company’s ownership structure.

- Click to explore a detailed breakdown of our findings in Japfa's financial health report.

- Explore Japfa's analyst forecasts in our growth report.

Seize The Opportunity

- Investigate our full lineup of 1,172 Asian Penny Stocks right here.

- Ready For A Different Approach? Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 20 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SGX:UD2

Japfa

An agri-food company, produces and sells protein staples, and packaged food products in Indonesia, Vietnam, India, Myanmar, and internationally.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Fair Value US$31.72|41.9% undervalued

KI

Community Contributor

EasyJet weirdly unloved by investors in spite of relatively attractive metrics

Fair Value UK£6.95|31.9% undervalued

PI

Community Contributor

HEXPOL AB: Sustained Long Term Growth, Stable Margins, and Strategic M&A

Fair Value SEK 122.27|24.9% undervalued

MA

Community Contributor