Advertisement

- Hong Kong

- /

- Capital Markets

- /

- SEHK:665

These Analysts Think Haitong International Securities Group Limited's (HKG:665) Sales Are Under Threat

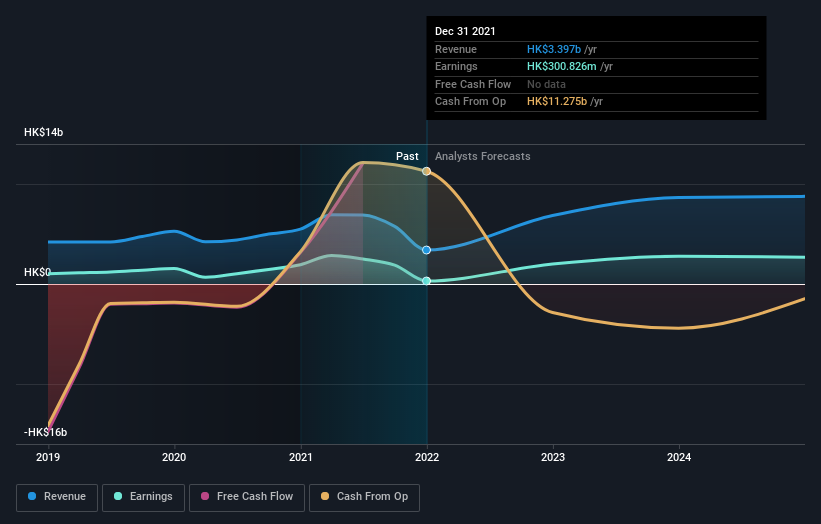

The latest analyst coverage could presage a bad day for Haitong International Securities Group Limited (HKG:665), with the analysts making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. This report focused on revenue estimates, and it looks as though the consensus view of the business has become substantially more conservative.

After the downgrade, the three analysts covering Haitong International Securities Group are now predicting revenues of HK$6.8b in 2022. If met, this would reflect a huge 101% improvement in sales compared to the last 12 months. Statutory earnings per share are presumed to jump 471% to HK$0.28. Previously, the analysts had been modelling revenues of HK$7.7b and earnings per share (EPS) of HK$0.31 in 2022. Indeed, we can see that analyst sentiment has declined measurably after the new consensus came out, with a measurable cut to revenue estimates and a minor downgrade to EPS estimates to boot.

View our latest analysis for Haitong International Securities Group

The consensus price target fell 5.4% to HK$2.31, with the weaker earnings outlook clearly leading analyst valuation estimates. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values Haitong International Securities Group at HK$3.21 per share, while the most bearish prices it at HK$1.73. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's clear from the latest estimates that Haitong International Securities Group's rate of growth is expected to accelerate meaningfully, with the forecast 101% annualised revenue growth to the end of 2022 noticeably faster than its historical growth of 4.0% p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 14% annually. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Haitong International Securities Group to grow faster than the wider industry.

The Bottom Line

The biggest issue in the new estimates is that analysts have reduced their earnings per share estimates, suggesting business headwinds lay ahead for Haitong International Securities Group. Unfortunately, analysts also downgraded their revenue estimates, although our data indicates revenues are expected to perform better than the wider market. Furthermore, there was a cut to the price target, suggesting that the latest news has led to more pessimism about the intrinsic value of the business. Given the stark change in sentiment, we'd understand if investors became more cautious on Haitong International Securities Group after today.

Worse, Haitong International Securities Group is labouring under a substantial debt burden, which - if today's forecasts prove accurate - the forecast downgrade could potentially exacerbate. See why we're concerned about Haitong International Securities Group's balance sheet by visiting our risks dashboard for free on our platform here.

We also provide an overview of the Haitong International Securities Group Board and CEO remuneration and length of tenure at the company, and whether insiders have been buying the stock, here.

Valuation is complex, but we're here to simplify it.

Discover if Haitong International Securities Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:665

Haitong International Securities Group

Haitong International Securities Group Limited provides financial products and services to corporate, institutional, and high-net worth worldwide.

Mediocre balance sheet with weak fundamentals.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor