- Hong Kong

- /

- Capital Markets

- /

- SEHK:6608

3 Companies Estimated To Be Trading Below Their Intrinsic Value In February 2025

Reviewed by Simply Wall St

As global markets navigate a period of volatility marked by fluctuating interest rates and competitive pressures in the technology sector, investors are keenly observing the impact on stock valuations. Amidst these dynamics, identifying companies trading below their intrinsic value can present opportunities for those looking to capitalize on potential market inefficiencies.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Alltop Technology (TPEX:3526) | NT$264.50 | NT$527.77 | 49.9% |

| Sichuan Injet Electric (SZSE:300820) | CN¥50.58 | CN¥101.01 | 49.9% |

| Gaming Realms (AIM:GMR) | £0.358 | £0.71 | 49.7% |

| GlobalData (AIM:DATA) | £1.78 | £3.55 | 49.9% |

| Bufab (OM:BUFAB) | SEK467.40 | SEK928.96 | 49.7% |

| EuroGroup Laminations (BIT:EGLA) | €2.604 | €5.17 | 49.6% |

| AeroEdge (TSE:7409) | ¥1749.00 | ¥3474.82 | 49.7% |

| GemPharmatech (SHSE:688046) | CN¥13.06 | CN¥25.94 | 49.7% |

| Prodways Group (ENXTPA:PWG) | €0.576 | €1.15 | 49.8% |

| Gold Royalty (NYSEAM:GROY) | US$1.32 | US$2.63 | 49.9% |

Let's take a closer look at a couple of our picks from the screened companies.

Mobvista (SEHK:1860)

Overview: Mobvista Inc., with a market cap of HK$10.90 billion, provides advertising and marketing technology services to support the development of the mobile internet ecosystem globally.

Operations: The company's revenue is derived from advertising and marketing technology services that facilitate the growth of the global mobile internet ecosystem.

Estimated Discount To Fair Value: 46.4%

Mobvista's earnings and revenue growth forecasts are robust, with earnings expected to grow 67.6% annually, outpacing the Hong Kong market. The company is trading at HK$8.49, significantly below its estimated fair value of HK$15.85, indicating potential undervaluation based on cash flows. Despite recent volatility in share price and large one-off items affecting financial results, Mobvista's revenue for Q3 2024 increased to US$416.46 million from US$269.37 million a year ago, supporting strong future prospects.

- Our growth report here indicates Mobvista may be poised for an improving outlook.

- Click here to discover the nuances of Mobvista with our detailed financial health report.

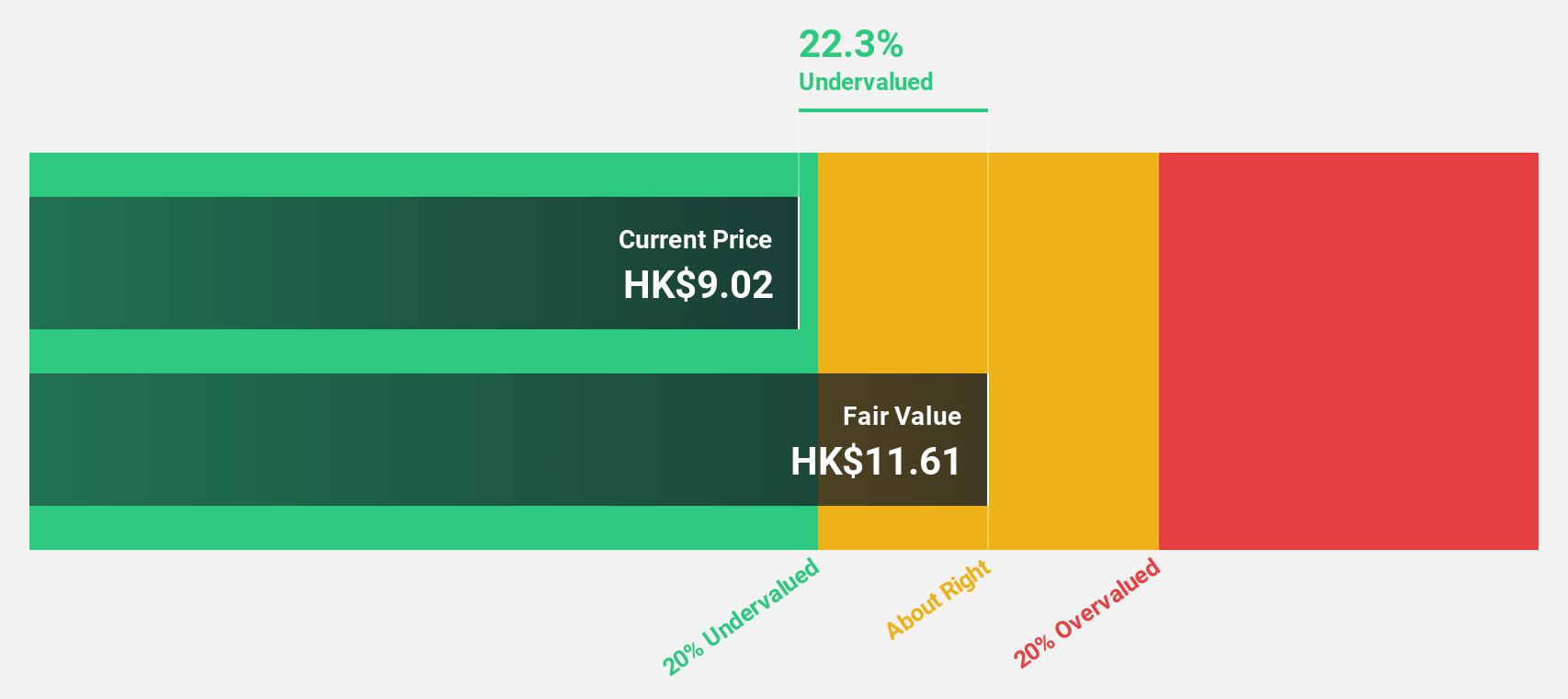

Bairong (SEHK:6608)

Overview: Bairong Inc. is a cloud-based AI turnkey services provider in China with a market cap of approximately HK$3.83 billion.

Operations: The company's revenue segment includes Data Processing, which generated CN¥2.76 billion.

Estimated Discount To Fair Value: 43.5%

Bairong is trading at HK$9.53, significantly below its estimated fair value of HK$16.88, suggesting it could be undervalued based on cash flows. Analysts predict the stock price may rise by 38.3%, and earnings are expected to grow 27.8% annually, outpacing the Hong Kong market's growth rate of 11.3%. However, profit margins have declined from last year and significant insider selling has occurred recently, which may warrant caution for investors.

- The analysis detailed in our Bairong growth report hints at robust future financial performance.

- Dive into the specifics of Bairong here with our thorough financial health report.

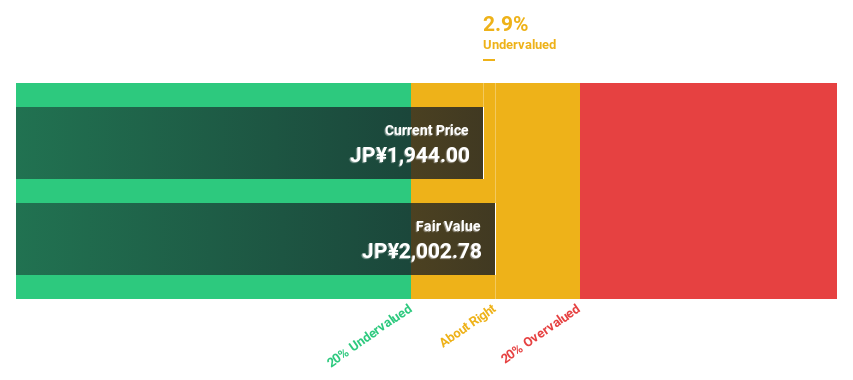

Aisan Industry (TSE:7283)

Overview: Aisan Industry Co., Ltd. manufactures and sells automotive parts both in Japan and internationally, with a market cap of ¥119.59 billion.

Operations: Aisan Industry Co., Ltd. generates revenue through the production and distribution of automotive components across domestic and international markets.

Estimated Discount To Fair Value: 10.4%

Aisan Industry is trading at ¥1,900, below its estimated fair value of ¥2,119.7, indicating potential undervaluation based on cash flows. Earnings are forecast to grow 21.3% annually, outpacing the JP market's 8% growth rate. However, the return on equity is expected to be low at 12.3% in three years and the company has an unstable dividend track record. Despite these concerns, revenue growth is projected to exceed market averages at 8.6% per year.

- Our earnings growth report unveils the potential for significant increases in Aisan Industry's future results.

- Click to explore a detailed breakdown of our findings in Aisan Industry's balance sheet health report.

Summing It All Up

- Click through to start exploring the rest of the 917 Undervalued Stocks Based On Cash Flows now.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bairong might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:6608

Flawless balance sheet and undervalued.

Market Insights

Community Narratives