Advertisement

- Hong Kong

- /

- Capital Markets

- /

- SEHK:174

Gemini Investments (Holdings) Limited's (HKG:174) Price Is Right But Growth Is Lacking

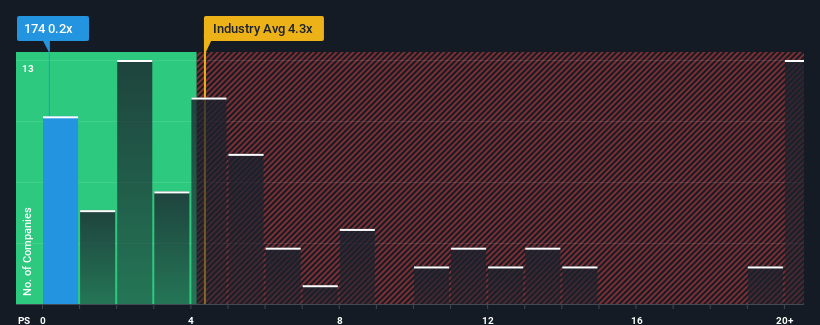

You may think that with a price-to-sales (or "P/S") ratio of 0.2x Gemini Investments (Holdings) Limited (HKG:174) is definitely a stock worth checking out, seeing as almost half of all the Capital Markets companies in Hong Kong have P/S ratios greater than 4.3x and even P/S above 13x aren't out of the ordinary. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so limited.

View our latest analysis for Gemini Investments (Holdings)

How Has Gemini Investments (Holdings) Performed Recently?

Revenue has risen at a steady rate over the last year for Gemini Investments (Holdings), which is generally not a bad outcome. Perhaps the market believes the recent revenue performance might fall short of industry figures in the near future, leading to a reduced P/S. Those who are bullish on Gemini Investments (Holdings) will be hoping that this isn't the case, so that they can pick up the stock at a lower valuation.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Gemini Investments (Holdings) will help you shine a light on its historical performance.How Is Gemini Investments (Holdings)'s Revenue Growth Trending?

There's an inherent assumption that a company should far underperform the industry for P/S ratios like Gemini Investments (Holdings)'s to be considered reasonable.

Taking a look back first, we see that the company managed to grow revenues by a handy 5.7% last year. Ultimately though, it couldn't turn around the poor performance of the prior period, with revenue shrinking 3.5% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Weighing that medium-term revenue trajectory against the broader industry's one-year forecast for expansion of 23% shows it's an unpleasant look.

In light of this, it's understandable that Gemini Investments (Holdings)'s P/S would sit below the majority of other companies. Nonetheless, there's no guarantee the P/S has reached a floor yet with revenue going in reverse. Even just maintaining these prices could be difficult to achieve as recent revenue trends are already weighing down the shares.

What We Can Learn From Gemini Investments (Holdings)'s P/S?

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Gemini Investments (Holdings) revealed its shrinking revenue over the medium-term is contributing to its low P/S, given the industry is set to grow. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises either. If recent medium-term revenue trends continue, it's hard to see the share price moving strongly in either direction in the near future under these circumstances.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Gemini Investments (Holdings) (at least 1 which can't be ignored), and understanding these should be part of your investment process.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:174

Gemini Investments (Holdings)

An investment holding company, engages in property investment and development, and other businesses in Hong Kong, the United States, and internationally.

Mediocre balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|36.3% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor