Advertisement

- Hong Kong

- /

- Consumer Services

- /

- SEHK:6068

Lacklustre Performance Is Driving Wisdom Education International Holdings Company Limited's (HKG:6068) 34% Price Drop

Wisdom Education International Holdings Company Limited (HKG:6068) shares have had a horrible month, losing 34% after a relatively good period beforehand. Indeed, the recent drop has reduced its annual gain to a relatively sedate 2.3% over the last twelve months.

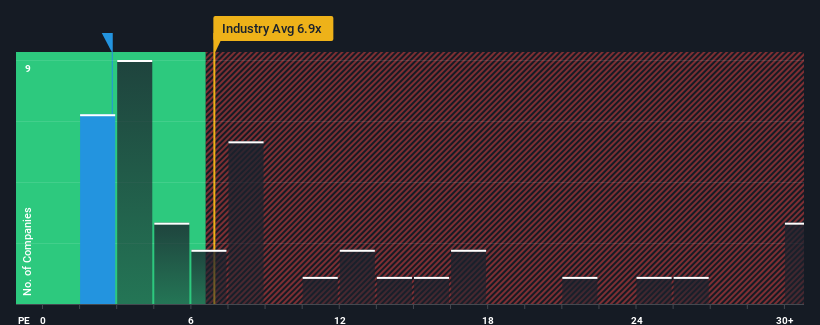

Even after such a large drop in price, Wisdom Education International Holdings may still be sending very bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 2.8x, since almost half of all companies in Hong Kong have P/E ratios greater than 10x and even P/E's higher than 19x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/E.

Wisdom Education International Holdings certainly has been doing a great job lately as it's been growing earnings at a really rapid pace. One possibility is that the P/E is low because investors think this strong earnings growth might actually underperform the broader market in the near future. If that doesn't eventuate, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

See our latest analysis for Wisdom Education International Holdings

Does Growth Match The Low P/E?

There's an inherent assumption that a company should far underperform the market for P/E ratios like Wisdom Education International Holdings' to be considered reasonable.

Taking a look back first, we see that the company grew earnings per share by an impressive 71% last year. Despite this strong recent growth, it's still struggling to catch up as its three-year EPS frustratingly shrank by 70% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Weighing that medium-term earnings trajectory against the broader market's one-year forecast for expansion of 20% shows it's an unpleasant look.

With this information, we are not surprised that Wisdom Education International Holdings is trading at a P/E lower than the market. However, we think shrinking earnings are unlikely to lead to a stable P/E over the longer term, which could set up shareholders for future disappointment. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

What We Can Learn From Wisdom Education International Holdings' P/E?

Wisdom Education International Holdings' P/E looks about as weak as its stock price lately. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Wisdom Education International Holdings maintains its low P/E on the weakness of its sliding earnings over the medium-term, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. If recent medium-term earnings trends continue, it's hard to see the share price moving strongly in either direction in the near future under these circumstances.

And what about other risks? Every company has them, and we've spotted 4 warning signs for Wisdom Education International Holdings (of which 1 shouldn't be ignored!) you should know about.

If these risks are making you reconsider your opinion on Wisdom Education International Holdings, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Wisdom Education International Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:6068

Wisdom Education International Holdings

An investment holding company, operates schools in the People’s Republic of China and Hong Kong.

Excellent balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|20.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.5% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|20.5% undervalued

CH

Community Contributor