- Hong Kong

- /

- Hospitality

- /

- SEHK:520

Investors Aren't Buying Xiabuxiabu Catering Management (China) Holdings Co., Ltd.'s (HKG:520) Revenues

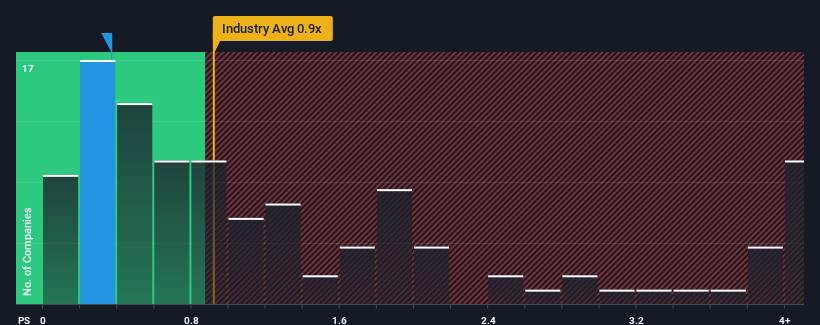

You may think that with a price-to-sales (or "P/S") ratio of 0.4x Xiabuxiabu Catering Management (China) Holdings Co., Ltd. (HKG:520) is a stock worth checking out, seeing as almost half of all the Hospitality companies in Hong Kong have P/S ratios greater than 0.9x and even P/S higher than 3x aren't out of the ordinary. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

See our latest analysis for Xiabuxiabu Catering Management (China) Holdings

What Does Xiabuxiabu Catering Management (China) Holdings' Recent Performance Look Like?

Recent times haven't been great for Xiabuxiabu Catering Management (China) Holdings as its revenue has been rising slower than most other companies. Perhaps the market is expecting the current trend of poor revenue growth to continue, which has kept the P/S suppressed. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Xiabuxiabu Catering Management (China) Holdings.What Are Revenue Growth Metrics Telling Us About The Low P/S?

Xiabuxiabu Catering Management (China) Holdings' P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

Taking a look back first, we see that the company managed to grow revenues by a handy 3.0% last year. Although, the latest three year period in total hasn't been as good as it didn't manage to provide any growth at all. Therefore, it's fair to say that revenue growth has been inconsistent recently for the company.

Looking ahead now, revenue is anticipated to climb by 20% each year during the coming three years according to the analysts following the company. That's shaping up to be materially lower than the 25% per annum growth forecast for the broader industry.

With this in consideration, its clear as to why Xiabuxiabu Catering Management (China) Holdings' P/S is falling short industry peers. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Key Takeaway

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Xiabuxiabu Catering Management (China) Holdings' analyst forecasts revealed that its inferior revenue outlook is contributing to its low P/S. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. The company will need a change of fortune to justify the P/S rising higher in the future.

The company's balance sheet is another key area for risk analysis. Take a look at our free balance sheet analysis for Xiabuxiabu Catering Management (China) Holdings with six simple checks on some of these key factors.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:520

Xiabuxiabu Catering Management (China) Holdings

An investment holding company, operates Chinese hotpot restaurants in the People’s Republic of China and internationally.

Undervalued with moderate growth potential.

Market Insights

Community Narratives