- Hong Kong

- /

- Hospitality

- /

- SEHK:520

Improved Revenues Required Before Xiabuxiabu Catering Management (China) Holdings Co., Ltd. (HKG:520) Stock's 30% Jump Looks Justified

Xiabuxiabu Catering Management (China) Holdings Co., Ltd. (HKG:520) shareholders are no doubt pleased to see that the share price has bounced 30% in the last month, although it is still struggling to make up recently lost ground. Still, the 30-day jump doesn't change the fact that longer term shareholders have seen their stock decimated by the 63% share price drop in the last twelve months.

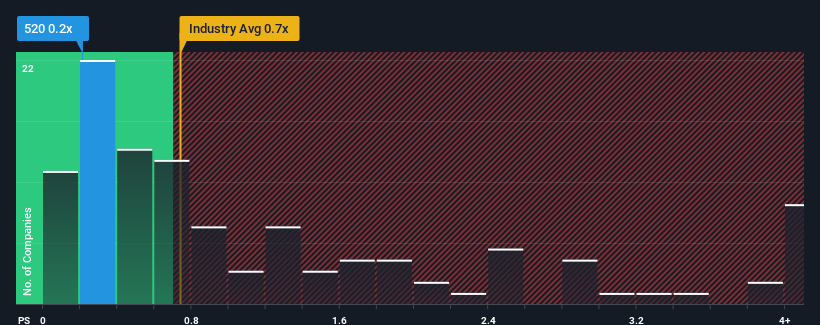

In spite of the firm bounce in price, Xiabuxiabu Catering Management (China) Holdings may still be sending bullish signals at the moment with its price-to-sales (or "P/S") ratio of 0.2x, since almost half of all companies in the Hospitality industry in Hong Kong have P/S ratios greater than 0.7x and even P/S higher than 3x are not unusual. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Xiabuxiabu Catering Management (China) Holdings

What Does Xiabuxiabu Catering Management (China) Holdings' P/S Mean For Shareholders?

Recent times haven't been great for Xiabuxiabu Catering Management (China) Holdings as its revenue has been rising slower than most other companies. The P/S ratio is probably low because investors think this lacklustre revenue performance isn't going to get any better. If you still like the company, you'd be hoping revenue doesn't get any worse and that you could pick up some stock while it's out of favour.

Want the full picture on analyst estimates for the company? Then our free report on Xiabuxiabu Catering Management (China) Holdings will help you uncover what's on the horizon.How Is Xiabuxiabu Catering Management (China) Holdings' Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as low as Xiabuxiabu Catering Management (China) Holdings' is when the company's growth is on track to lag the industry.

Retrospectively, the last year delivered virtually the same number to the company's top line as the year before. This isn't what shareholders were looking for as it means they've been left with a 17% decline in revenue over the last three years in total. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Looking ahead now, revenue is anticipated to climb by 11% per year during the coming three years according to the eight analysts following the company. That's shaping up to be materially lower than the 14% each year growth forecast for the broader industry.

With this information, we can see why Xiabuxiabu Catering Management (China) Holdings is trading at a P/S lower than the industry. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

What We Can Learn From Xiabuxiabu Catering Management (China) Holdings' P/S?

The latest share price surge wasn't enough to lift Xiabuxiabu Catering Management (China) Holdings' P/S close to the industry median. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We've established that Xiabuxiabu Catering Management (China) Holdings maintains its low P/S on the weakness of its forecast growth being lower than the wider industry, as expected. Shareholders' pessimism on the revenue prospects for the company seems to be the main contributor to the depressed P/S. The company will need a change of fortune to justify the P/S rising higher in the future.

Before you take the next step, you should know about the 1 warning sign for Xiabuxiabu Catering Management (China) Holdings that we have uncovered.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:520

Xiabuxiabu Catering Management (China) Holdings

An investment holding company, operates Chinese hotpot restaurants in the People’s Republic of China and internationally.

Undervalued with moderate growth potential.

Market Insights

Community Narratives