Fairwood Holdings Limited (HKG:52) is reducing its dividend from last year's comparable payment to HK$0.40 on the 6th of October. The yield is still above the industry average at 5.0%.

Check out our latest analysis for Fairwood Holdings

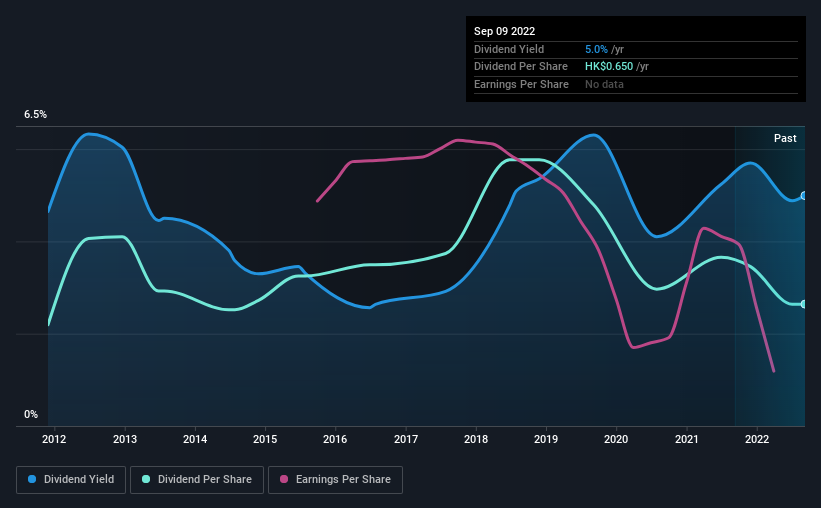

Fairwood Holdings Is Paying Out More Than It Is Earning

A big dividend yield for a few years doesn't mean much if it can't be sustained. Prior to this announcement, the company was paying out 197% of what it was earning, however the dividend was quite comfortably covered by free cash flows at a cash payout ratio of only 17%. Given that the dividend is a cash outflow, we think that cash is more important than accounting measures of profit when assessing the dividend, so this is a mitigating factor.

If the company can't turn things around, EPS could fall by 27.2% over the next year. Assuming the dividend continues along recent trends, we believe the payout ratio could reach 265%, which could put the dividend under pressure if earnings don't start to improve.

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. Since 2012, the dividend has gone from HK$0.54 total annually to HK$0.65. This implies that the company grew its distributions at a yearly rate of about 1.9% over that duration. The dividend has seen some fluctuations in the past, so even though the dividend was raised this year, we should remember that it has been cut in the past.

The Dividend Has Limited Growth Potential

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. Fairwood Holdings' EPS has fallen by approximately 27% per year during the past five years. This steep decline can indicate that the business is going through a tough time, which could constrain its ability to pay a larger dividend each year in the future.

Fairwood Holdings' Dividend Doesn't Look Sustainable

In summary, dividends being cut isn't ideal, however it can bring the payment into a more sustainable range. The payments haven't been particularly stable and we don't see huge growth potential, but with the dividend well covered by cash flows it could prove to be reliable over the short term. This company is not in the top tier of income providing stocks.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. However, there are other things to consider for investors when analysing stock performance. Case in point: We've spotted 4 warning signs for Fairwood Holdings (of which 1 doesn't sit too well with us!) you should know about. Is Fairwood Holdings not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:52

Fairwood Holdings

An investment holding company, operates fast food restaurants.

Excellent balance sheet slight.

Market Insights

Community Narratives