Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Café de Coral Holdings Limited (HKG:341) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Café de Coral Holdings

What Is Café de Coral Holdings's Debt?

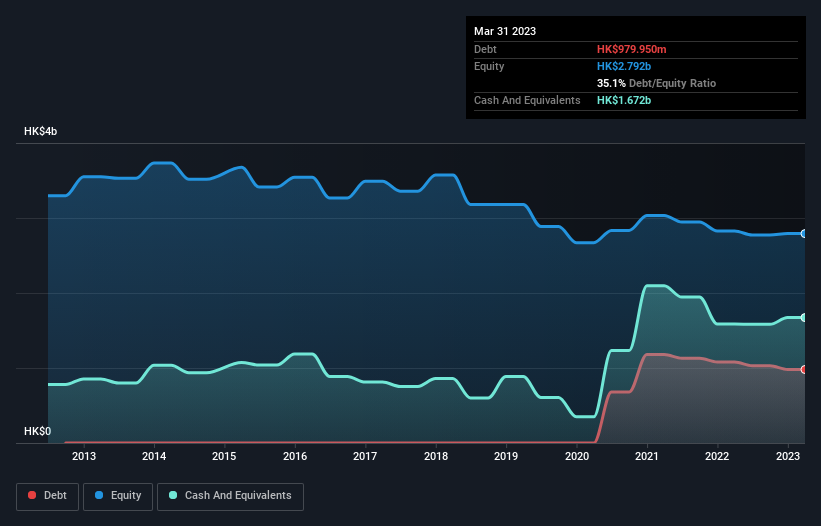

You can click the graphic below for the historical numbers, but it shows that Café de Coral Holdings had HK$980.0m of debt in March 2023, down from HK$1.08b, one year before. However, it does have HK$1.67b in cash offsetting this, leading to net cash of HK$692.0m.

How Healthy Is Café de Coral Holdings' Balance Sheet?

According to the last reported balance sheet, Café de Coral Holdings had liabilities of HK$2.78b due within 12 months, and liabilities of HK$1.60b due beyond 12 months. On the other hand, it had cash of HK$1.67b and HK$142.5m worth of receivables due within a year. So it has liabilities totalling HK$2.57b more than its cash and near-term receivables, combined.

This deficit isn't so bad because Café de Coral Holdings is worth HK$6.39b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt. While it does have liabilities worth noting, Café de Coral Holdings also has more cash than debt, so we're pretty confident it can manage its debt safely.

Notably, Café de Coral Holdings's EBIT launched higher than Elon Musk, gaining a whopping 123% on last year. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Café de Coral Holdings can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Café de Coral Holdings has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Happily for any shareholders, Café de Coral Holdings actually produced more free cash flow than EBIT over the last two years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Summing Up

While Café de Coral Holdings does have more liabilities than liquid assets, it also has net cash of HK$692.0m. The cherry on top was that in converted 490% of that EBIT to free cash flow, bringing in HK$775m. So we don't have any problem with Café de Coral Holdings's use of debt. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of Café de Coral Holdings's earnings per share history for free.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:341

Café de Coral Holdings

An investment holding company, engages in the operation of quick service restaurants and casual dining chains in Hong Kong and Mainland China.

Proven track record and fair value.