Advertisement

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

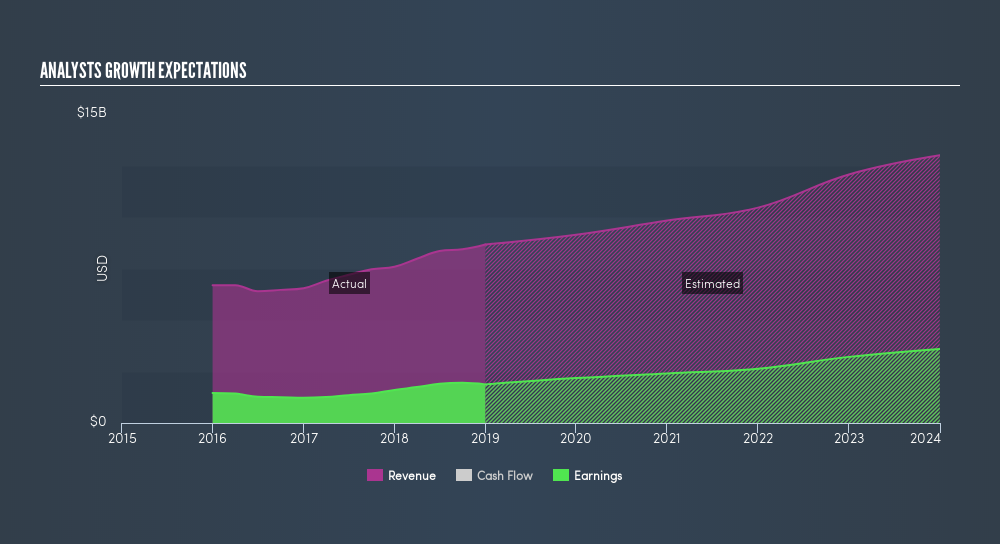

Based on Sands China Ltd.'s (HKG:1928) earnings update in December 2018, analyst consensus outlook appear cautiously optimistic, as a 16% increase in profits is expected in the upcoming year, against the past 5-year average growth rate of -9.8%. Presently, with latest-twelve-month earnings at US$1.9b, we should see this growing to US$2.2b by 2020. In this article, I've outline a few earnings growth rates to give you a sense of the market sentiment for Sands China in the longer term. For those interested in more of an analysis of the company, you can research its fundamentals here.

See our latest analysis for Sands China

Exciting times ahead?

Over the next three years, it seems the consensus view of the 25 analysts covering 1928 is skewed towards the positive sentiment. Broker analysts tend to forecast up to three years ahead due to a lack of clarity around the business trajectory beyond this. To reduce the year-on-year volatility of analyst earnings forecast, I've inserted a line of best fit through the expected earnings figures to determine the annual growth rate from the slope of the line.

By 2022, 1928's earnings should reach US$2.6b, from current levels of US$1.9b, resulting in an annual growth rate of 10%. This leads to an EPS of $0.33 in the final year of projections relative to the current EPS of $0.23. Margins are currently sitting at 22%, which is expected to expand to 25% by 2022.

Next Steps:

Future outlook is only one aspect when you're building an investment case for a stock. For Sands China, I've compiled three pertinent aspects you should further examine:

- Financial Health: Does it have a healthy balance sheet? Take a look at our free balance sheet analysis with six simple checks on key factors like leverage and risk.

- Valuation: What is Sands China worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether Sands China is currently mispriced by the market.

- Other High-Growth Alternatives : Are there other high-growth stocks you could be holding instead of Sands China? Explore our interactive list of stocks with large growth potential to get an idea of what else is out there you may be missing!

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About SEHK:1928

Sands China

Develops, owns, and operates integrated resorts and casinos in Macao.

Moderate growth potential and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

36 followersusers have followed this narrative

6 commentsusers have commented on this narrative

10 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1918.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5190.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

114 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

952 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative