Advertisement

- Hong Kong

- /

- Consumer Services

- /

- SEHK:1890

China Kepei (SEHK:1890) Net Profit Margin Falls to 40%, Challenging Defensiveness Narrative

Simply Wall St

Reviewed by Simply Wall St

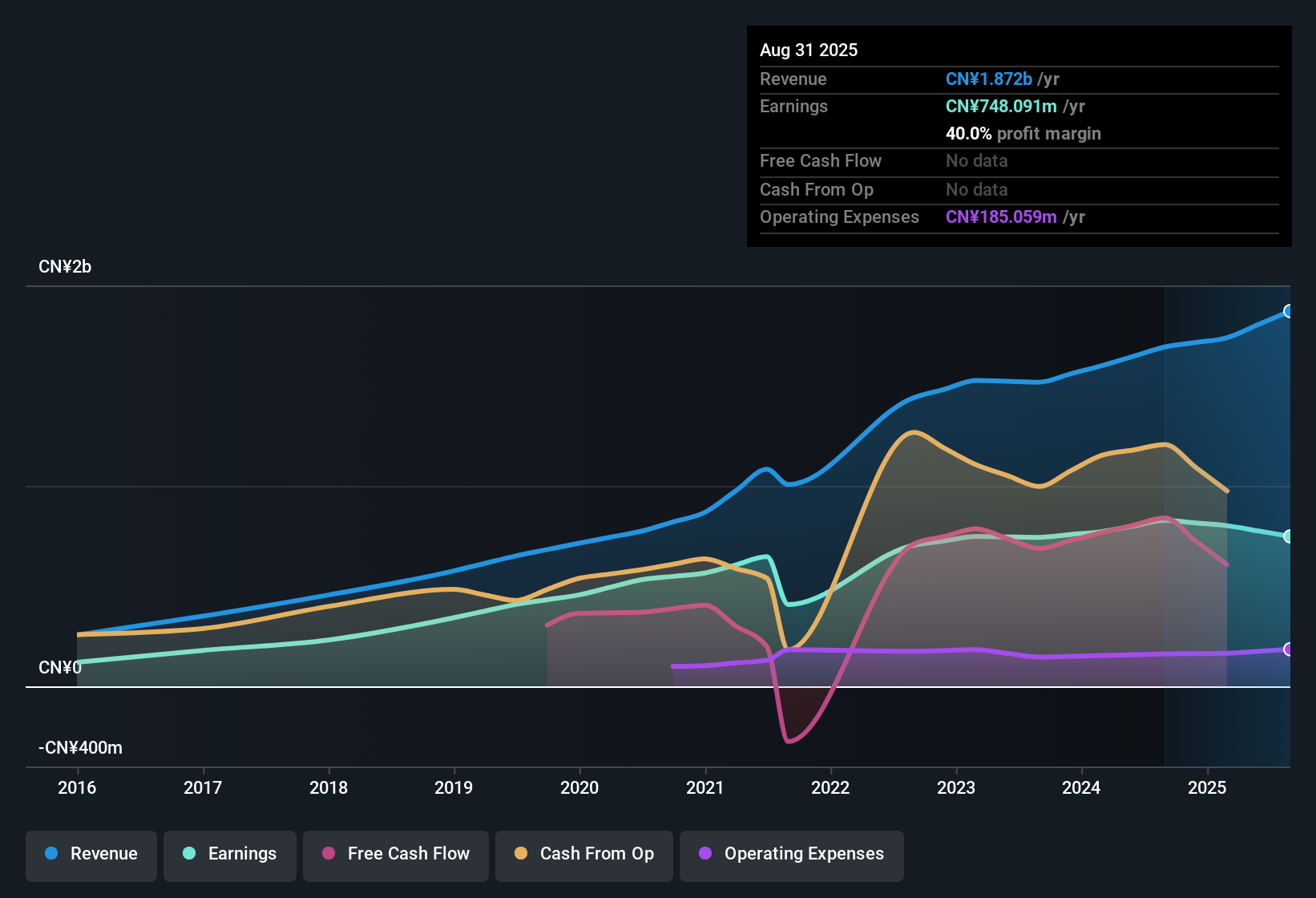

China Kepei Education Group (SEHK:1890) just released its FY 2025 interim figures, reporting revenue of 918.2 million CNY and basic EPS of 0.21 CNY. Looking at the recent history, revenue has ranged from 820.9 million CNY up to 918.2 million CNY across the last three half-year periods. Basic EPS has swung between 0.19 and 0.22 CNY. Net income has also fluctuated, showing that profit margins have been under some pressure alongside changes in earnings per share.

See our full analysis for China Kepei Education Group.Next, we line up these headline numbers with the prevailing narratives in the market to see which stories gain traction and which face new questions.

Curious how numbers become stories that shape markets? Explore Community Narratives

Net Profit Margins Fall to 40%

- Over the trailing twelve months, net profit margins stood at 40%, a notable drop from 48.9% in the prior year. This highlights real pressure on profitability that was not fully apparent from headline net income and EPS numbers earlier in the article.

- The prevailing market analysis points out that, while long-term average annual earnings growth reached 8.2% over the past five years, the most recent twelve months saw negative earnings growth. This contradicts the bullish view that Kepei's profit engine is reliably defensive and shows that even a niche not targeted by regulatory crackdowns can face cyclical softness.

- Profitability has become more volatile, driven by a squeeze on margins in the latest period.

- This margin compression underpins skepticism from cautious investors that growth and returns may not be as durable as historical averages suggest.

Discounted Valuation Versus Peers

- China Kepei trades at a price-to-earnings multiple of 3.5x, well below peer (5x) and industry (7.3x) averages, and current market price (HK$1.45) reflects an 81.1% discount to DCF fair value (HK$7.68). This signals substantial undervaluation not captured in just earnings trends.

- What sets this apart, analysts note, is that such a wide valuation gap can either reflect genuine market pessimism on near-term growth or offer a margin of safety to value investors attracted by consistently high historical earnings quality.

- Despite the recent negative turn in earnings growth, the low absolute and relative multiples could make the stock appealing to bargain hunters focused on longer-term averages.

- The market may be waiting for proof of stabilization before rerating. At these levels, even a modest improvement in profitability could drive significant upside.

Dividend Track Record: Instability Persists

- Dividend consistency remains a weak spot, as the company is flagged for an unstable payout record. This contrasts with otherwise high-quality reported earnings over the past twelve months.

- From a market perspective, this pattern of unreliable shareholder returns directly challenges the notion that historically strong profit margins would automatically translate into steady payouts.

- Investors looking for predictable income may view the inconsistent dividend as a red flag, despite the group’s historically robust net income.

- The unstable dividend history stands out as a minor but tangible risk, even as core earnings quality remains strong overall.

See how the rest of the market is weighing these trends and what investors think happens next: See what the community is saying about China Kepei Education Group

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on China Kepei Education Group's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

China Kepei’s inconsistent profit growth and unstable dividend history signal potential risks for investors relying on steady shareholder returns.

If reliable income is important to you, check out these 1922 dividend stocks with yields > 3% to discover companies delivering more consistent payouts and stronger dividend track records.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1890

China Kepei Education Group

An investment holding company, provides private vocational education services focusing on profession-oriented and vocational education in the People’s Republic of China.

Good value with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

139 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

931 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative