Advertisement

- Hong Kong

- /

- Consumer Services

- /

- SEHK:1890

China Kepei Education Group Limited's (HKG:1890) Shares Lagging The Market But So Is The Business

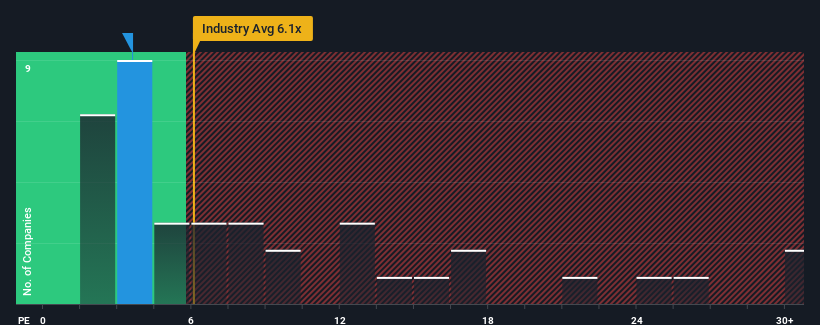

When close to half the companies in Hong Kong have price-to-earnings ratios (or "P/E's") above 10x, you may consider China Kepei Education Group Limited (HKG:1890) as a highly attractive investment with its 3.6x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

There hasn't been much to differentiate China Kepei Education Group's and the market's earnings growth lately. It might be that many expect the mediocre earnings performance to degrade, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could pick up some stock while it's out of favour.

See our latest analysis for China Kepei Education Group

Does Growth Match The Low P/E?

There's an inherent assumption that a company should far underperform the market for P/E ratios like China Kepei Education Group's to be considered reasonable.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 3.1% last year. The latest three year period has also seen a 26% overall rise in EPS, aided somewhat by its short-term performance. So we can start by confirming that the company has actually done a good job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 5.8% each year during the coming three years according to the four analysts following the company. With the market predicted to deliver 16% growth per year, the company is positioned for a weaker earnings result.

In light of this, it's understandable that China Kepei Education Group's P/E sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Bottom Line On China Kepei Education Group's P/E

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

As we suspected, our examination of China Kepei Education Group's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Many other vital risk factors can be found on the company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for China Kepei Education Group with six simple checks.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1890

China Kepei Education Group

An investment holding company, provides private vocational education services focusing on profession-oriented and vocational education in the People’s Republic of China.

Undervalued with adequate balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|28.6% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.5% undervalued

AG

Community Contributor