- Hong Kong

- /

- Hospitality

- /

- SEHK:1488

Here's Why Best Food Holding Company Limited's (HKG:1488) CEO Might See A Pay Rise Soon

Key Insights

- Best Food Holding to hold its Annual General Meeting on 20th of June

- Total pay for CEO Bruce Wang includes CN¥1.49m salary

- The total compensation is 46% less than the average for the industry

- Best Food Holding's EPS grew by 13% over the past three years while total shareholder return over the past three years was 31%

Shareholders will be pleased by the robust performance of Best Food Holding Company Limited (HKG:1488) recently and this will be kept in mind in the upcoming AGM on 20th of June. They will probably be more interested in hearing the board discuss future initiatives to further improve the business as they vote on resolutions such as executive remuneration. Here is our take on why we think CEO compensation is fair and may even warrant a raise.

View our latest analysis for Best Food Holding

How Does Total Compensation For Bruce Wang Compare With Other Companies In The Industry?

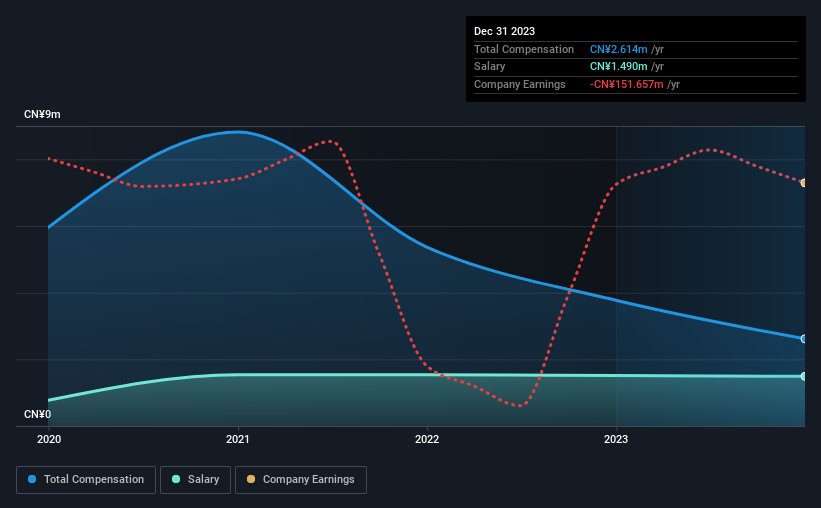

According to our data, Best Food Holding Company Limited has a market capitalization of HK$1.3b, and paid its CEO total annual compensation worth CN¥2.6m over the year to December 2023. We note that's a decrease of 31% compared to last year. Notably, the salary which is CN¥1.49m, represents a considerable chunk of the total compensation being paid.

On comparing similar companies from the Hong Kong Hospitality industry with market caps ranging from HK$781m to HK$3.1b, we found that the median CEO total compensation was CN¥4.8m. This suggests that Bruce Wang is paid below the industry median.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | CN¥1.5m | CN¥1.5m | 57% |

| Other | CN¥1.1m | CN¥2.3m | 43% |

| Total Compensation | CN¥2.6m | CN¥3.8m | 100% |

On an industry level, roughly 86% of total compensation represents salary and 14% is other remuneration. Best Food Holding pays a modest slice of remuneration through salary, as compared to the broader industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Best Food Holding Company Limited's Growth

Over the past three years, Best Food Holding Company Limited has seen its earnings per share (EPS) grow by 13% per year. Its revenue is up 15% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's also good to see decent revenue growth in the last year, suggesting the business is healthy and growing. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Best Food Holding Company Limited Been A Good Investment?

With a total shareholder return of 31% over three years, Best Food Holding Company Limited shareholders would, in general, be reasonably content. But they probably wouldn't be so happy as to think the CEO should be paid more than is normal, for companies around this size.

To Conclude...

The company's overall performance, while not bad, could be better. Assuming the business continues to grow at a good clip, few shareholders would raise any objections to the CEO's remuneration. Rather, investors would more likely want to engage on discussions related to key strategic initiatives and future growth opportunities for the company and set their longer-term expectations.

CEO compensation can have a massive impact on performance, but it's just one element. That's why we did some digging and identified 1 warning sign for Best Food Holding that you should be aware of before investing.

Important note: Best Food Holding is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

If you're looking to trade Best Food Holding, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Best Food Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1488

Best Food Holding

An investment holding company, operates a chain of restaurants in the People's Republic of China.

Very low with weak fundamentals.

Market Insights

Community Narratives