- Hong Kong

- /

- Consumer Services

- /

- SEHK:1161

Water Oasis Group Limited's (HKG:1161) CEO Might Not Expect Shareholders To Be So Generous This Year

Key Insights

- Water Oasis Group will host its Annual General Meeting on 20th of January

- Total pay for CEO Alan Tam includes HK$5.28m salary

- Total compensation is 332% above industry average

- Water Oasis Group's three-year loss to shareholders was 33% while its EPS was down 26% over the past three years

Shareholders will probably not be too impressed with the underwhelming results at Water Oasis Group Limited (HKG:1161) recently. Shareholders will be interested in what the board will have to say about turning performance around at the next AGM on 20th of January. This will be also be a chance where they can challenge the board on company direction and vote on resolutions such as executive remuneration. From our analysis, we think CEO compensation may need a review in light of the recent performance.

View our latest analysis for Water Oasis Group

How Does Total Compensation For Alan Tam Compare With Other Companies In The Industry?

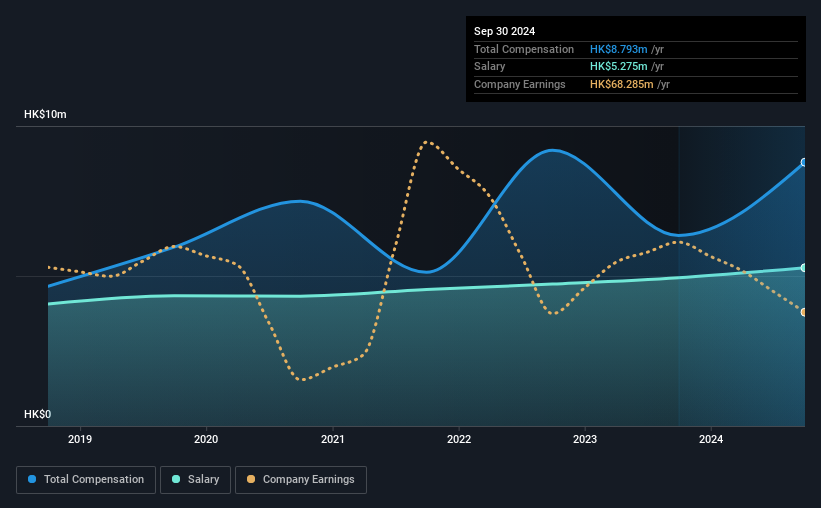

At the time of writing, our data shows that Water Oasis Group Limited has a market capitalization of HK$565m, and reported total annual CEO compensation of HK$8.8m for the year to September 2024. We note that's an increase of 38% above last year. We note that the salary of HK$5.28m makes up a sizeable portion of the total compensation received by the CEO.

For comparison, other companies in the Hong Kong Consumer Services industry with market capitalizations below HK$1.6b, reported a median total CEO compensation of HK$2.0m. This suggests that Alan Tam is paid more than the median for the industry. What's more, Alan Tam holds HK$8.1m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | HK$5.3m | HK$4.9m | 60% |

| Other | HK$3.5m | HK$1.4m | 40% |

| Total Compensation | HK$8.8m | HK$6.3m | 100% |

On an industry level, around 84% of total compensation represents salary and 16% is other remuneration. Water Oasis Group pays a modest slice of remuneration through salary, as compared to the broader industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Water Oasis Group Limited's Growth Numbers

Over the last three years, Water Oasis Group Limited has shrunk its earnings per share by 26% per year. In the last year, its revenue changed by just 0.7%.

The decline in EPS is a bit concerning. And the flat revenue is seriously uninspiring. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Water Oasis Group Limited Been A Good Investment?

The return of -33% over three years would not have pleased Water Oasis Group Limited shareholders. So shareholders would probably want the company to be less generous with CEO compensation.

To Conclude...

Not only have shareholders not seen a favorable return on their investment, but the business hasn't performed well either. Few shareholders would be willing to award the CEO with a pay raise. At the upcoming AGM, they can question the management's plans and strategies to turn performance around and reassess their investment thesis in regards to the company.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. We did our research and spotted 4 warning signs for Water Oasis Group that investors should look into moving forward.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

Valuation is complex, but we're here to simplify it.

Discover if Water Oasis Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1161

Water Oasis Group

Operates beauty services centers in Hong Kong, Macau, and the People's Republic of China.

Excellent balance sheet average dividend payer.

Market Insights

Community Narratives