- Hong Kong

- /

- Consumer Services

- /

- SEHK:1161

Increases to Water Oasis Group Limited's (HKG:1161) CEO Compensation Might Cool off for now

Despite Water Oasis Group Limited's (HKG:1161) share price growing positively in the past few years, the per-share earnings growth has not grown to investors' expectations, suggesting that there could be other factors at play driving the share price. These concerns will be at the front of shareholders' minds as they go into the AGM coming up on 19 April 2021. They will be able to influence managerial decisions through the exercise of their voting power on resolutions, such as CEO remuneration and other matters, which may influence future company prospects. In our analysis below, we show why shareholders may consider holding off a raise for the CEO's compensation until company performance improves.

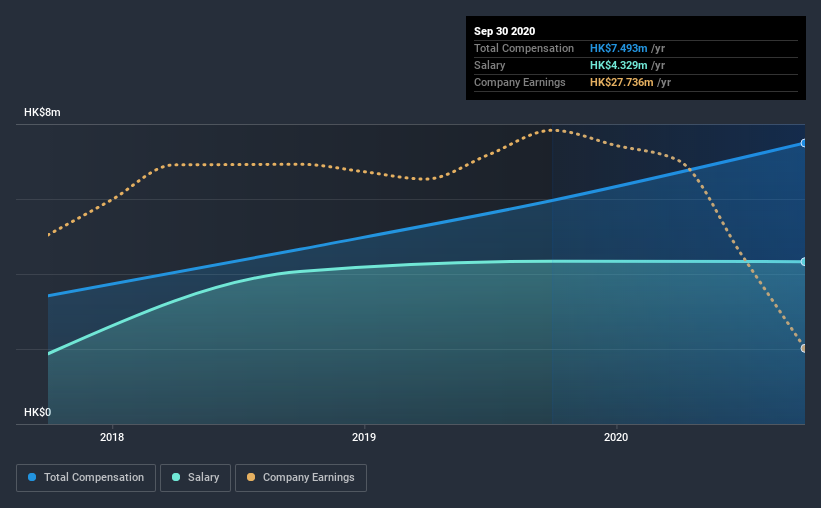

View our latest analysis for Water Oasis Group

Comparing Water Oasis Group Limited's CEO Compensation With the industry

According to our data, Water Oasis Group Limited has a market capitalization of HK$565m, and paid its CEO total annual compensation worth HK$7.5m over the year to September 2020. Notably, that's an increase of 26% over the year before. In particular, the salary of HK$4.33m, makes up a fairly large portion of the total compensation being paid to the CEO.

In comparison with other companies in the industry with market capitalizations under HK$1.6b, the reported median total CEO compensation was HK$1.3m. This suggests that Alan Tam is paid more than the median for the industry. What's more, Alan Tam holds HK$4.9m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | HK$4.3m | HK$4.3m | 58% |

| Other | HK$3.2m | HK$1.6m | 42% |

| Total Compensation | HK$7.5m | HK$6.0m | 100% |

Talking in terms of the industry, salary represented approximately 90% of total compensation out of all the companies we analyzed, while other remuneration made up 10% of the pie. It's interesting to note that Water Oasis Group allocates a smaller portion of compensation to salary in comparison to the broader industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Water Oasis Group Limited's Growth Numbers

Over the last three years, Water Oasis Group Limited has shrunk its earnings per share by 23% per year. It saw its revenue drop 30% over the last year.

Few shareholders would be pleased to read that EPS have declined. This is compounded by the fact revenue is actually down on last year. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Water Oasis Group Limited Been A Good Investment?

Water Oasis Group Limited has served shareholders reasonably well, with a total return of 30% over three years. But they would probably prefer not to see CEO compensation far in excess of the median.

To Conclude...

Despite the positive returns on shareholders' investments, the fact that earnings have failed to grow makes us skeptical about whether these returns will continue. The upcoming AGM will provide shareholders the opportunity to revisit the company’s remuneration policies and evaluate if the board’s judgement and decision-making is aligned with that of the company’s shareholders.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. That's why we did some digging and identified 3 warning signs for Water Oasis Group that investors should think about before committing capital to this stock.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

If you decide to trade Water Oasis Group, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

If you're looking to trade Water Oasis Group, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Water Oasis Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1161

Water Oasis Group

Operates beauty services centers in Hong Kong, Macau, and the People's Republic of China.

Excellent balance sheet, good value and pays a dividend.