Advertisement

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Summit Ascent Holdings Limited (HKG:102) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

Our analysis indicates that 102 is potentially overvalued!

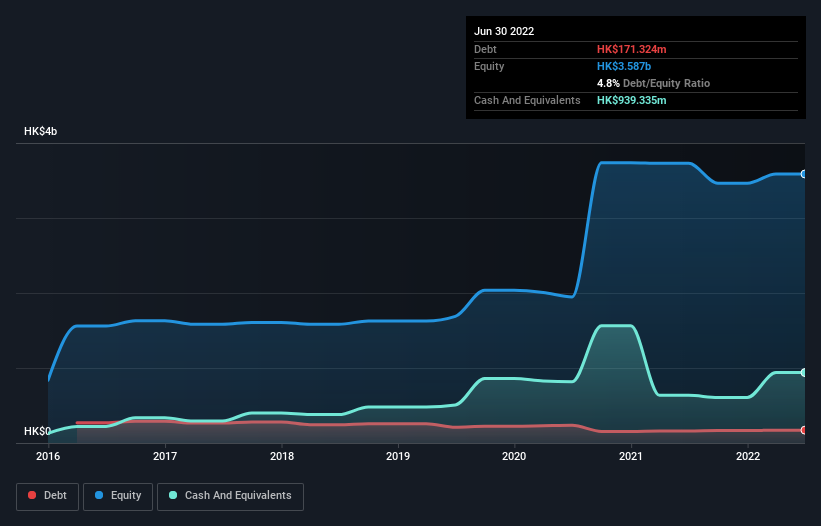

What Is Summit Ascent Holdings's Net Debt?

The image below, which you can click on for greater detail, shows that at June 2022 Summit Ascent Holdings had debt of HK$171.3m, up from HK$159.8m in one year. However, it does have HK$939.3m in cash offsetting this, leading to net cash of HK$768.0m.

A Look At Summit Ascent Holdings' Liabilities

Zooming in on the latest balance sheet data, we can see that Summit Ascent Holdings had liabilities of HK$65.1m due within 12 months and liabilities of HK$203.3m due beyond that. Offsetting these obligations, it had cash of HK$939.3m as well as receivables valued at HK$38.7m due within 12 months. So it actually has HK$709.6m more liquid assets than total liabilities.

This surplus strongly suggests that Summit Ascent Holdings has a rock-solid balance sheet (and the debt is of no concern whatsoever). With this in mind one could posit that its balance sheet means the company is able to handle some adversity. Simply put, the fact that Summit Ascent Holdings has more cash than debt is arguably a good indication that it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Summit Ascent Holdings will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Summit Ascent Holdings wasn't profitable at an EBIT level, but managed to grow its revenue by 14%, to HK$279m. We usually like to see faster growth from unprofitable companies, but each to their own.

So How Risky Is Summit Ascent Holdings?

While Summit Ascent Holdings lost money on an earnings before interest and tax (EBIT) level, it actually generated positive free cash flow HK$21m. So taking that on face value, and considering the net cash situation, we don't think that the stock is too risky in the near term. There's no doubt the next few years will be crucial to how the business matures. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 2 warning signs for Summit Ascent Holdings (1 is potentially serious) you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:102

Summit Ascent Holdings

Summit Ascent Holdings Limited, an investment holding company, engages in the operation of hotel and gaming business.

Adequate balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|58.8% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|17.5% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|2.4% undervalued

RO

Community Contributor