Advertisement

Kiddieland International (HKG:3830) Is Carrying A Fair Bit Of Debt

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Kiddieland International Limited (HKG:3830) makes use of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Kiddieland International

What Is Kiddieland International's Net Debt?

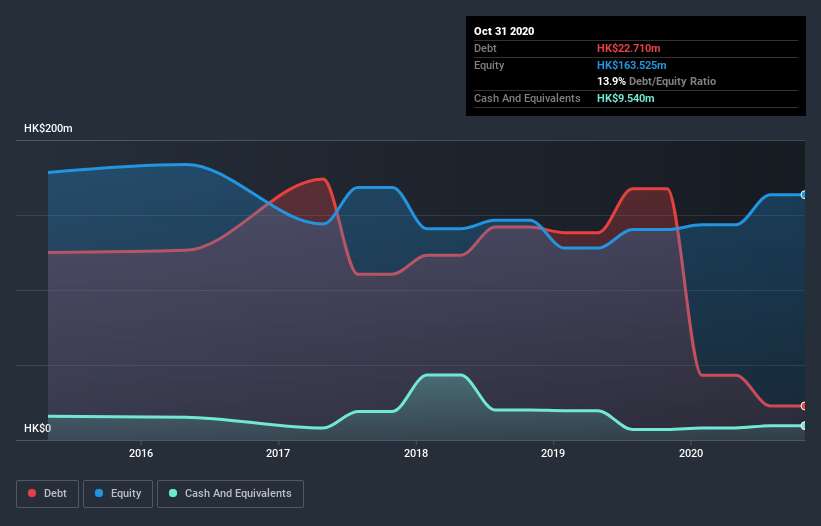

The image below, which you can click on for greater detail, shows that Kiddieland International had debt of HK$22.7m at the end of October 2020, a reduction from HK$167.5m over a year. However, because it has a cash reserve of HK$9.54m, its net debt is less, at about HK$13.2m.

A Look At Kiddieland International's Liabilities

Zooming in on the latest balance sheet data, we can see that Kiddieland International had liabilities of HK$73.4m due within 12 months and liabilities of HK$22.2m due beyond that. On the other hand, it had cash of HK$9.54m and HK$101.2m worth of receivables due within a year. So it actually has HK$15.1m more liquid assets than total liabilities.

This short term liquidity is a sign that Kiddieland International could probably pay off its debt with ease, as its balance sheet is far from stretched. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Kiddieland International will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year Kiddieland International had a loss before interest and tax, and actually shrunk its revenue by 7.1%, to HK$282m. We would much prefer see growth.

Caveat Emptor

Over the last twelve months Kiddieland International produced an earnings before interest and tax (EBIT) loss. To be specific the EBIT loss came in at HK$893k. Looking on the brighter side, the business has adequate liquid assets, which give it time to grow and develop before its debt becomes a near-term issue. And on top of that, it booked free cash flow of HK$48m and profit of HK$166m over the last year. This one is a bit too risky for our liking. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 2 warning signs for Kiddieland International you should be aware of, and 1 of them can't be ignored.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you’re looking to trade Kiddieland International, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Kiddieland International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:3830

Kiddieland International

An investment holding company, manufactures and distributes plastic toy products and laboratory equipment in the United States, Europe, the Asia Pacific and Oceania, and the People's Republic of China.

Flawless balance sheet low.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor