Samsonite International (SEHK:1910) Leverages Product Innovation and DTC Growth to Overcome Sales Decline

Reviewed by Simply Wall St

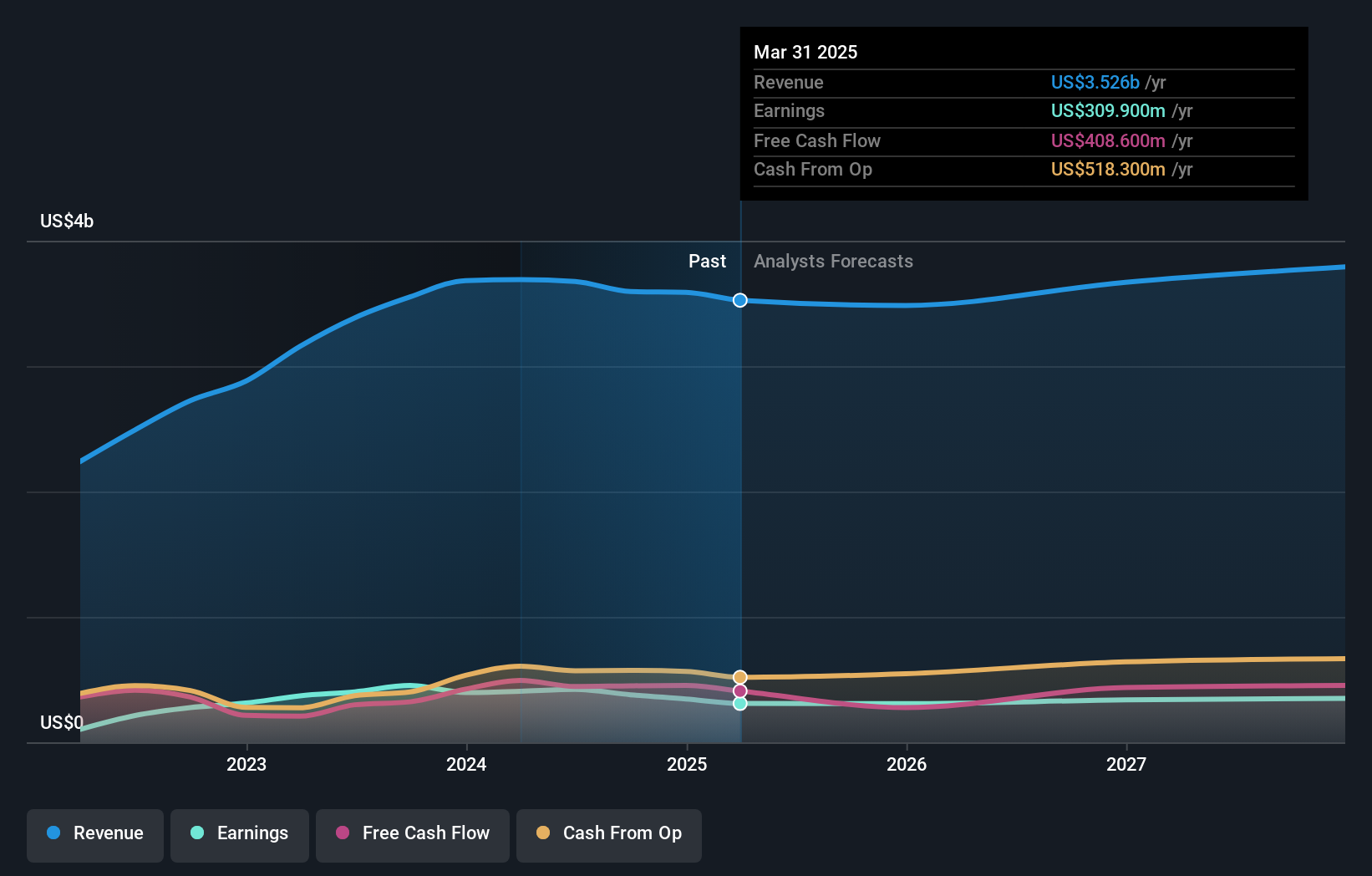

Samsonite International (SEHK:1910) continues to showcase its financial profile, with recent developments highlighting a $94 million cash flow, an increase from the previous year, and strong performance in North America and Europe. However, the company faces challenges such as a 6.8% decline in net sales due to a tough promotional environment, particularly affecting the Tumi brand in North America and Asia. The following report will explore Samsonite's competitive advantages, potential growth strategies, and the key risks that could impact its success.

Competitive Advantages That Elevate Samsonite International

Samsonite International has demonstrated a solid financial profile, underscored by its strong margin profile and cash flow. CEO Kyle Gendreau noted that the company maintained a high margin, with cash flow reaching $94 million, an increase of $5 million from the previous year. This highlights effective cost management and operational efficiency. The company's performance in North America and Europe is particularly noteworthy, with the Samsonite brand showing resilience and Tumi experiencing growth in Europe, as reported by Gendreau. This geographic strength supports its market presence and positions it well for future growth. Additionally, Samsonite's asset-light business model enhances its financial health, enabling strong cash generation and supporting shareholder returns. The company's Price-To-Earnings Ratio of 10.2x presents it as a competitive player relative to a peer average of 16.6x, though slightly above the Hong Kong Luxury industry average of 9.6x.

Challenges Constraining Samsonite International's Potential

Samsonite faces challenges that could impede its growth. The company experienced a 6.8% decline in net sales, attributed to a challenging promotional environment, particularly in India. This environment has pressured the Tumi brand, especially in North America and Asia, where slower consumer traffic and spending have affected performance. Furthermore, fixed SG&A expenses have increased as a percentage of sales, indicating potential inefficiencies. The company's net debt to equity ratio stands at 73.9%, which is relatively high and could pose financial risks if not managed effectively. Additionally, the earnings growth forecast of 3.8% per year lags behind the Hong Kong market's 11.3%, suggesting potential competitive pressures.

Potential Strategies for Leveraging Growth and Competitive Advantage

Opportunities abound for Samsonite, particularly in expanding its direct-to-consumer (DTC) channels. The company has seen a 3% increase in year-to-date DTC sales, with e-commerce sites up by 7.3% across all regions. This focus on DTC channels, including strategic store openings, enhances consumer engagement. Product innovation within the Tumi brand offers additional growth prospects, with new lightweight hardside collections and non-travel segments poised to drive market penetration. Samsonite's commitment to sustainability, aiming to reduce Scope 3 emissions by 52% by 2030, aligns with consumer demand for eco-friendly products and could further bolster its market appeal.

Key Risks and Challenges That Could Impact Samsonite International's Success

Samsonite faces several external threats that could impact its success. Softer consumer sentiment in key markets such as China and India poses a risk to sales growth, compounded by broader economic uncertainties. Intense competition and promotional pressures, particularly in India, threaten profit margins and market share, necessitating strategic pricing adjustments. Additionally, potential changes in trade tariffs and supply chain disruptions present risks to cost structures and operational efficiency. These factors require proactive management to mitigate their impact on Samsonite's long-term growth trajectory.

Conclusion

Samsonite International's strong financial health, characterized by a high margin profile and significant cash flow, underscores its effective cost management and operational efficiency, positioning it well for sustained growth in North America and Europe. However, challenges such as declining net sales and increased SG&A expenses highlight areas requiring strategic attention, particularly in India and Asia, to maintain competitive advantage. The company's focus on expanding direct-to-consumer channels and product innovation, alongside its commitment to sustainability, offers promising avenues for future growth. While Samsonite's Price-To-Earnings Ratio of 10.2x indicates it is a competitive player compared to peers, it remains slightly above the Hong Kong Luxury industry average, indicating the need for careful management of financial and operational risks to capitalize on its market positioning.

Taking Advantage

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

```New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1910

Samsonite International

Engages in the design, manufacture, sourcing, and distribution of travel luggage bags in North America, Asia, Europe, and Latin America.

Average dividend payer and fair value.