Advertisement

- Hong Kong

- /

- Professional Services

- /

- SEHK:6113

UTS Marketing Solutions Holdings Limited's (HKG:6113) Has Had A Decent Run On The Stock market: Are Fundamentals In The Driver's Seat?

Most readers would already know that UTS Marketing Solutions Holdings' (HKG:6113) stock increased by 7.5% over the past three months. We wonder if and what role the company's financials play in that price change as a company's long-term fundamentals usually dictate market outcomes. In this article, we decided to focus on UTS Marketing Solutions Holdings' ROE.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

View our latest analysis for UTS Marketing Solutions Holdings

How To Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for UTS Marketing Solutions Holdings is:

17% = RM14m ÷ RM80m (Based on the trailing twelve months to June 2020).

The 'return' refers to a company's earnings over the last year. Another way to think of that is that for every HK$1 worth of equity, the company was able to earn HK$0.17 in profit.

What Has ROE Got To Do With Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

UTS Marketing Solutions Holdings' Earnings Growth And 17% ROE

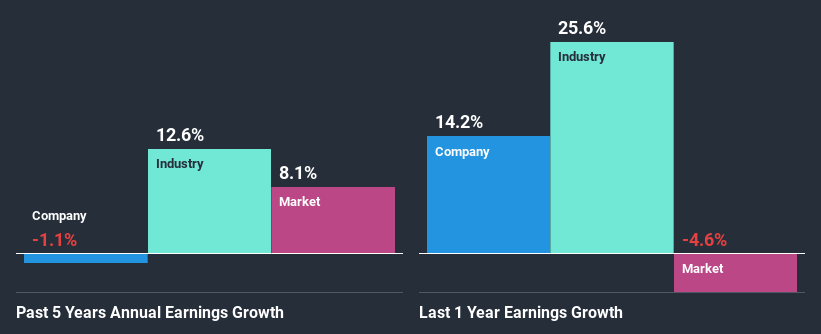

To start with, UTS Marketing Solutions Holdings' ROE looks acceptable. Further, the company's ROE compares quite favorably to the industry average of 10%. Given the circumstances, we can't help but wonder why UTS Marketing Solutions Holdings saw little to no growth in the past five years. Therefore, there could be some other aspects that could potentially be preventing the company from growing. Such as, the company pays out a huge portion of its earnings as dividends, or is faced with competitive pressures.

We then compared UTS Marketing Solutions Holdings' net income growth with the industry and found that the average industry growth rate was 13% in the same period.

Earnings growth is a huge factor in stock valuation. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. If you're wondering about UTS Marketing Solutions Holdings''s valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is UTS Marketing Solutions Holdings Efficiently Re-investing Its Profits?

With a high three-year median payout ratio of 74% (implying that the company keeps only 26% of its income) of its business to reinvest into its business), most of UTS Marketing Solutions Holdings' profits are being paid to shareholders, which explains the absence of growth in earnings.

In addition, UTS Marketing Solutions Holdings has been paying dividends over a period of three years suggesting that keeping up dividend payments is way more important to the management even if it comes at the cost of business growth.

Summary

On the whole, we do feel that UTS Marketing Solutions Holdings has some positive attributes. However, while the company does have a high ROE, its earnings growth number is quite disappointing. This can be blamed on the fact that it reinvests only a small portion of its profits and pays out the rest as dividends. Up till now, we've only made a short study of the company's growth data. You can do your own research on UTS Marketing Solutions Holdings and see how it has performed in the past by looking at this FREE detailed graph of past earnings, revenue and cash flows.

When trading UTS Marketing Solutions Holdings or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if BitStrat Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:6113

BitStrat Holdings

An investment holding company, provides outbound telemarketing services and contact center facilities in Malaysia.

Excellent balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor