Advertisement

- Hong Kong

- /

- Commercial Services

- /

- SEHK:257

Should You Investigate China Everbright Environment Group Limited (HKG:257) At HK$3.11?

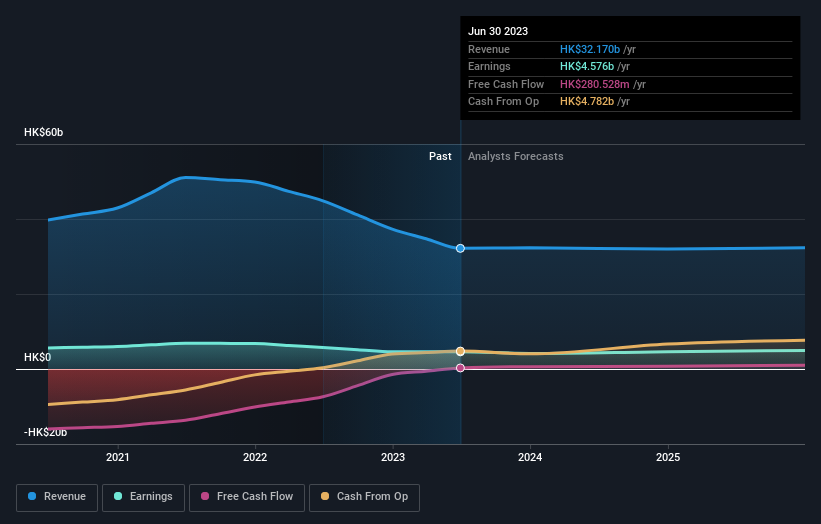

China Everbright Environment Group Limited (HKG:257), might not be a large cap stock, but it led the SEHK gainers with a relatively large price hike in the past couple of weeks. The recent rally in share prices has nudged the company in the right direction, though it still falls short of its yearly peak. With many analysts covering the mid-cap stock, we may expect any price-sensitive announcements have already been factored into the stock’s share price. But what if there is still an opportunity to buy? Today we will analyse the most recent data on China Everbright Environment Group’s outlook and valuation to see if the opportunity still exists.

View our latest analysis for China Everbright Environment Group

Is China Everbright Environment Group Still Cheap?

China Everbright Environment Group appears to be overvalued by 39% at the moment, based on our discounted cash flow valuation. The stock is currently priced at HK$3.11 on the market compared to our intrinsic value of HK$2.24. This means that the opportunity to buy China Everbright Environment Group at a good price has disappeared! Another thing to keep in mind is that China Everbright Environment Group’s share price is quite stable relative to the market, as indicated by its low beta. This means that if you believe the current share price should move towards its intrinsic value over time, a low beta could suggest it is not likely to reach that level anytime soon, and once it’s there, it may be hard to fall back down into an attractive buying range again.

What kind of growth will China Everbright Environment Group generate?

Investors looking for growth in their portfolio may want to consider the prospects of a company before buying its shares. Although value investors would argue that it’s the intrinsic value relative to the price that matter the most, a more compelling investment thesis would be high growth potential at a cheap price. However, with a relatively muted profit growth of 4.5% expected over the next couple of years, growth doesn’t seem like a key driver for a buy decision for China Everbright Environment Group, at least in the short term.

What This Means For You

Are you a shareholder? 257’s future growth appears to have been factored into the current share price, with shares trading above its fair value. However, this brings up another question – is now the right time to sell? If you believe 257 should trade below its current price, selling high and buying it back up again when its price falls towards its real value can be profitable. But before you make this decision, take a look at whether its fundamentals have changed.

Are you a potential investor? If you’ve been keeping tabs on 257 for some time, now may not be the best time to enter into the stock. The price has surpassed its true value, which means there’s no upside from mispricing. However, the positive outlook means it’s worth diving deeper into other factors in order to take advantage of the next price drop.

In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. When we did our research, we found 2 warning signs for China Everbright Environment Group (1 makes us a bit uncomfortable!) that we believe deserve your full attention.

If you are no longer interested in China Everbright Environment Group, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:257

China Everbright Environment Group

An investment holding company, provides environmental solutions worldwide.

Good value average dividend payer.

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|65.7% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|14.9% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|35.4% undervalued

DA

Community Contributor

Product Refresh And Global Expansion Will Empower Future Market Leadership

Fair Value US$202.60|21.0% undervalued

AN

Based on Analyst Price Targets