- Hong Kong

- /

- Construction

- /

- SEHK:8535

Vistar Holdings' (HKG:8535) Returns On Capital Not Reflecting Well On The Business

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. Having said that, from a first glance at Vistar Holdings (HKG:8535) we aren't jumping out of our chairs at how returns are trending, but let's have a deeper look.

Return On Capital Employed (ROCE): What Is It?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. To calculate this metric for Vistar Holdings, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.032 = HK$5.0m ÷ (HK$273m - HK$117m) (Based on the trailing twelve months to September 2023).

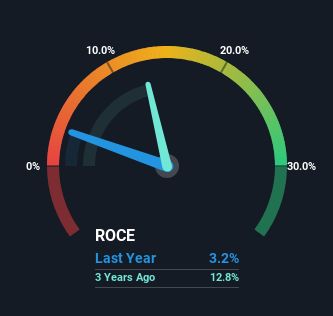

Thus, Vistar Holdings has an ROCE of 3.2%. In absolute terms, that's a low return and it also under-performs the Construction industry average of 7.6%.

See our latest analysis for Vistar Holdings

Historical performance is a great place to start when researching a stock so above you can see the gauge for Vistar Holdings' ROCE against it's prior returns. If you're interested in investigating Vistar Holdings' past further, check out this free graph covering Vistar Holdings' past earnings, revenue and cash flow.

What Can We Tell From Vistar Holdings' ROCE Trend?

On the surface, the trend of ROCE at Vistar Holdings doesn't inspire confidence. Over the last five years, returns on capital have decreased to 3.2% from 32% five years ago. And considering revenue has dropped while employing more capital, we'd be cautious. If this were to continue, you might be looking at a company that is trying to reinvest for growth but is actually losing market share since sales haven't increased.

Another thing to note, Vistar Holdings has a high ratio of current liabilities to total assets of 43%. This effectively means that suppliers (or short-term creditors) are funding a large portion of the business, so just be aware that this can introduce some elements of risk. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

The Bottom Line

From the above analysis, we find it rather worrisome that returns on capital and sales for Vistar Holdings have fallen, meanwhile the business is employing more capital than it was five years ago. Investors haven't taken kindly to these developments, since the stock has declined 68% from where it was five years ago. That being the case, unless the underlying trends revert to a more positive trajectory, we'd consider looking elsewhere.

If you want to know some of the risks facing Vistar Holdings we've found 4 warning signs (2 are a bit concerning!) that you should be aware of before investing here.

While Vistar Holdings isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:8535

Vistar Holdings

An investment holding company, provides electrical and mechanical engineering services in Hong Kong.

Excellent balance sheet low.

Market Insights

Community Narratives