We Think EVA Precision Industrial Holdings (HKG:838) Can Stay On Top Of Its Debt

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, EVA Precision Industrial Holdings Limited (HKG:838) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

Check out the opportunities and risks within the HK Machinery industry.

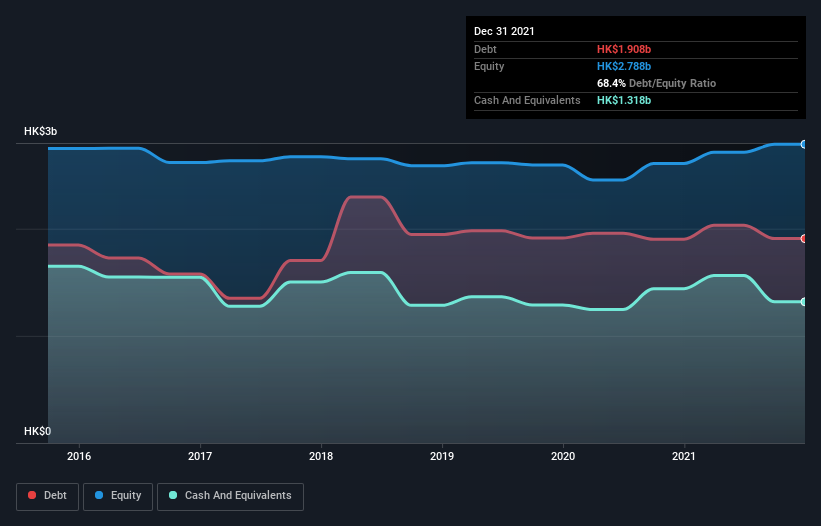

How Much Debt Does EVA Precision Industrial Holdings Carry?

As you can see below, EVA Precision Industrial Holdings had HK$2.10b of debt, at June 2022, which is about the same as the year before. You can click the chart for greater detail. On the flip side, it has HK$1.32b in cash leading to net debt of about HK$783.3m.

How Strong Is EVA Precision Industrial Holdings' Balance Sheet?

The latest balance sheet data shows that EVA Precision Industrial Holdings had liabilities of HK$3.28b due within a year, and liabilities of HK$619.8m falling due after that. Offsetting these obligations, it had cash of HK$1.32b as well as receivables valued at HK$1.67b due within 12 months. So its liabilities total HK$905.7m more than the combination of its cash and short-term receivables.

This deficit isn't so bad because EVA Precision Industrial Holdings is worth HK$2.18b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

We'd say that EVA Precision Industrial Holdings's moderate net debt to EBITDA ratio ( being 1.6), indicates prudence when it comes to debt. And its strong interest cover of 15.1 times, makes us even more comfortable. In addition to that, we're happy to report that EVA Precision Industrial Holdings has boosted its EBIT by 52%, thus reducing the spectre of future debt repayments. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine EVA Precision Industrial Holdings's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, EVA Precision Industrial Holdings reported free cash flow worth 2.2% of its EBIT, which is really quite low. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Our View

EVA Precision Industrial Holdings's interest cover was a real positive on this analysis, as was its EBIT growth rate. But truth be told its conversion of EBIT to free cash flow had us nibbling our nails. Considering this range of data points, we think EVA Precision Industrial Holdings is in a good position to manage its debt levels. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. Of course, we wouldn't say no to the extra confidence that we'd gain if we knew that EVA Precision Industrial Holdings insiders have been buying shares: if you're on the same wavelength, you can find out if insiders are buying by clicking this link.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if EVA Precision Industrial Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:838

EVA Precision Industrial Holdings

An investment holding company, provides precision manufacturing services in the People’s Republic of China, Vietnam, and Mexico.

Undervalued with excellent balance sheet and pays a dividend.