- Hong Kong

- /

- Construction

- /

- SEHK:8316

China Hongbao Holdings Limited's (HKG:8316) 42% Cheaper Price Remains In Tune With Revenues

China Hongbao Holdings Limited (HKG:8316) shares have retraced a considerable 42% in the last month, reversing a fair amount of their solid recent performance. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 57% loss during that time.

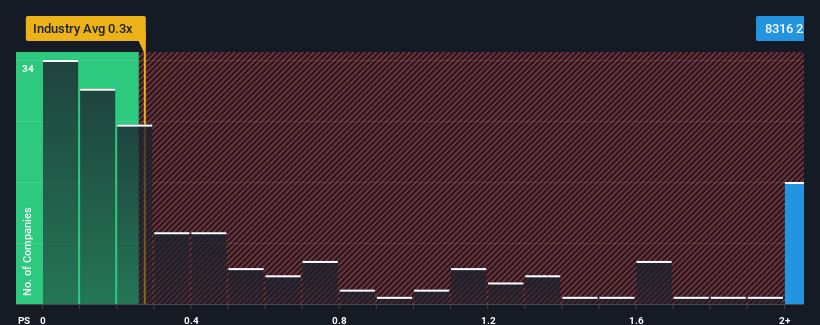

Even after such a large drop in price, when almost half of the companies in Hong Kong's Construction industry have price-to-sales ratios (or "P/S") below 0.3x, you may still consider China Hongbao Holdings as a stock not worth researching with its 2.5x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

See our latest analysis for China Hongbao Holdings

What Does China Hongbao Holdings' Recent Performance Look Like?

For example, consider that China Hongbao Holdings' financial performance has been poor lately as its revenue has been in decline. One possibility is that the P/S is high because investors think the company will still do enough to outperform the broader industry in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on China Hongbao Holdings' earnings, revenue and cash flow.Is There Enough Revenue Growth Forecasted For China Hongbao Holdings?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like China Hongbao Holdings' to be considered reasonable.

Retrospectively, the last year delivered a frustrating 38% decrease to the company's top line. However, a few very strong years before that means that it was still able to grow revenue by an impressive 61% in total over the last three years. Although it's been a bumpy ride, it's still fair to say the revenue growth recently has been more than adequate for the company.

When compared to the industry's one-year growth forecast of 9.2%, the most recent medium-term revenue trajectory is noticeably more alluring

In light of this, it's understandable that China Hongbao Holdings' P/S sits above the majority of other companies. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

What We Can Learn From China Hongbao Holdings' P/S?

A significant share price dive has done very little to deflate China Hongbao Holdings' very lofty P/S. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

It's no surprise that China Hongbao Holdings can support its high P/S given the strong revenue growth its experienced over the last three-year is superior to the current industry outlook. At this stage investors feel the potential continued revenue growth in the future is great enough to warrant an inflated P/S. If recent medium-term revenue trends continue, it's hard to see the share price falling strongly in the near future under these circumstances.

Before you take the next step, you should know about the 5 warning signs for China Hongbao Holdings (3 shouldn't be ignored!) that we have uncovered.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:8316

China Hongbao Holdings

An investment holding company, operates as a foundation subcontractor for private and public sectors in Hong Kong and People’s Republic of China.

Low with weak fundamentals.

Market Insights

Community Narratives