Advertisement

- Hong Kong

- /

- Construction

- /

- SEHK:750

Investors Could Be Concerned With China Shuifa Singyes Energy Holdings' (HKG:750) Returns On Capital

If you're looking at a mature business that's past the growth phase, what are some of the underlying trends that pop up? When we see a declining return on capital employed (ROCE) in conjunction with a declining base of capital employed, that's often how a mature business shows signs of aging. This indicates to us that the business is not only shrinking the size of its net assets, but its returns are falling as well. Having said that, after a brief look, China Shuifa Singyes Energy Holdings (HKG:750) we aren't filled with optimism, but let's investigate further.

Return On Capital Employed (ROCE): What Is It?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. Analysts use this formula to calculate it for China Shuifa Singyes Energy Holdings:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

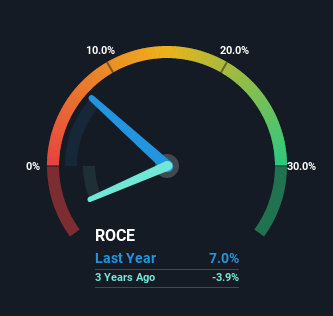

0.07 = CN¥567m ÷ (CN¥15b - CN¥6.5b) (Based on the trailing twelve months to December 2021).

So, China Shuifa Singyes Energy Holdings has an ROCE of 7.0%. On its own that's a low return on capital but it's in line with the industry's average returns of 7.1%.

See our latest analysis for China Shuifa Singyes Energy Holdings

Above you can see how the current ROCE for China Shuifa Singyes Energy Holdings compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free report for China Shuifa Singyes Energy Holdings.

What The Trend Of ROCE Can Tell Us

There is reason to be cautious about China Shuifa Singyes Energy Holdings, given the returns are trending downwards. About five years ago, returns on capital were 8.9%, however they're now substantially lower than that as we saw above. And on the capital employed front, the business is utilizing roughly the same amount of capital as it was back then. Companies that exhibit these attributes tend to not be shrinking, but they can be mature and facing pressure on their margins from competition. If these trends continue, we wouldn't expect China Shuifa Singyes Energy Holdings to turn into a multi-bagger.

While on the subject, we noticed that the ratio of current liabilities to total assets has risen to 44%, which has impacted the ROCE. If current liabilities hadn't increased as much as they did, the ROCE could actually be even lower. What this means is that in reality, a rather large portion of the business is being funded by the likes of the company's suppliers or short-term creditors, which can bring some risks of its own.

Our Take On China Shuifa Singyes Energy Holdings' ROCE

In summary, it's unfortunate that China Shuifa Singyes Energy Holdings is generating lower returns from the same amount of capital. It should come as no surprise then that the stock has fallen 62% over the last five years, so it looks like investors are recognizing these changes. That being the case, unless the underlying trends revert to a more positive trajectory, we'd consider looking elsewhere.

One final note, you should learn about the 3 warning signs we've spotted with China Shuifa Singyes Energy Holdings (including 1 which can't be ignored) .

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:750

China Shuifa Singyes Energy Holdings

An investment holding company, designs, fabricates, and installs conventional curtain walls in the People’s Republic of China.

Slightly overvalued with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor