Advertisement

Here's Why Sany Heavy Equipment International Holdings (HKG:631) Can Manage Its Debt Responsibly

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Sany Heavy Equipment International Holdings Company Limited (HKG:631) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Sany Heavy Equipment International Holdings

What Is Sany Heavy Equipment International Holdings's Net Debt?

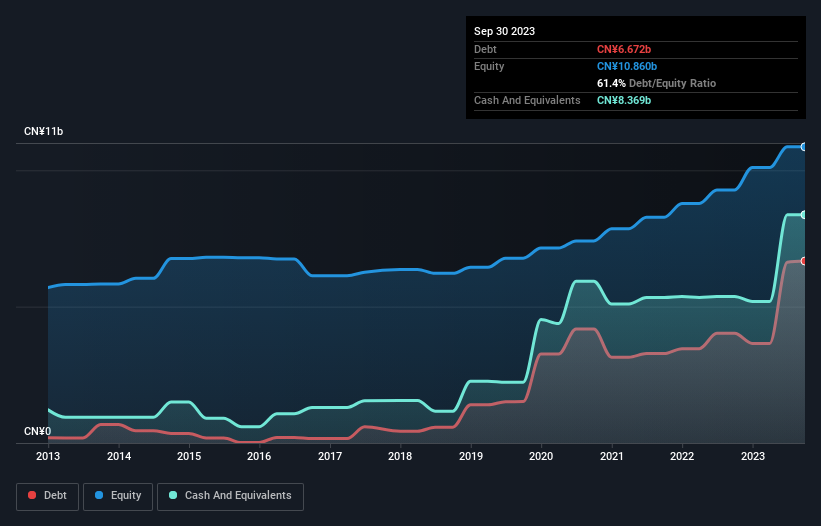

As you can see below, at the end of June 2023, Sany Heavy Equipment International Holdings had CN¥6.67b of debt, up from CN¥4.02b a year ago. Click the image for more detail. But it also has CN¥8.37b in cash to offset that, meaning it has CN¥1.70b net cash.

How Healthy Is Sany Heavy Equipment International Holdings' Balance Sheet?

We can see from the most recent balance sheet that Sany Heavy Equipment International Holdings had liabilities of CN¥18.5b falling due within a year, and liabilities of CN¥6.59b due beyond that. On the other hand, it had cash of CN¥8.37b and CN¥10.7b worth of receivables due within a year. So its liabilities total CN¥6.01b more than the combination of its cash and short-term receivables.

Sany Heavy Equipment International Holdings has a market capitalization of CN¥20.9b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt. Despite its noteworthy liabilities, Sany Heavy Equipment International Holdings boasts net cash, so it's fair to say it does not have a heavy debt load!

Better yet, Sany Heavy Equipment International Holdings grew its EBIT by 110% last year, which is an impressive improvement. If maintained that growth will make the debt even more manageable in the years ahead. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Sany Heavy Equipment International Holdings's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While Sany Heavy Equipment International Holdings has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. In the last three years, Sany Heavy Equipment International Holdings created free cash flow amounting to 2.5% of its EBIT, an uninspiring performance. That limp level of cash conversion undermines its ability to manage and pay down debt.

Summing Up

While Sany Heavy Equipment International Holdings does have more liabilities than liquid assets, it also has net cash of CN¥1.70b. And it impressed us with its EBIT growth of 110% over the last year. So we are not troubled with Sany Heavy Equipment International Holdings's debt use. Of course, we wouldn't say no to the extra confidence that we'd gain if we knew that Sany Heavy Equipment International Holdings insiders have been buying shares: if you're on the same wavelength, you can find out if insiders are buying by clicking this link.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:631

Sany Heavy Equipment International Holdings

Manufactures and sells mining and logistics equipment, electricity, power station project products, petroleum and new energy manufacturing equipment, spare parts, and related services.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor