Gemilang International (HKG:6163) Is Experiencing Growth In Returns On Capital

There are a few key trends to look for if we want to identify the next multi-bagger. Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. So when we looked at Gemilang International (HKG:6163) and its trend of ROCE, we really liked what we saw.

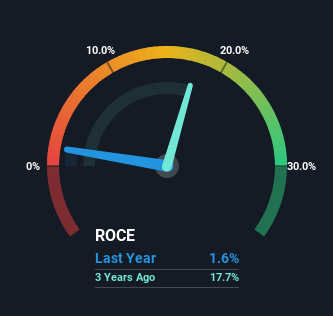

Return On Capital Employed (ROCE): What Is It?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Gemilang International is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.016 = US$324k ÷ (US$36m - US$15m) (Based on the trailing twelve months to April 2023).

Therefore, Gemilang International has an ROCE of 1.6%. In absolute terms, that's a low return and it also under-performs the Machinery industry average of 6.9%.

View our latest analysis for Gemilang International

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating Gemilang International's past further, check out this free graph of past earnings, revenue and cash flow.

SWOT Analysis for Gemilang International

- Debt is well covered by .

- Interest payments on debt are not well covered.

- Current share price is above our estimate of fair value.

- Has sufficient cash runway for more than 3 years based on current free cash flows.

- Lack of analyst coverage makes it difficult to determine 6163's earnings prospects.

- Debt is not well covered by operating cash flow.

What Does the ROCE Trend For Gemilang International Tell Us?

Gemilang International has broken into the black (profitability) and we're sure it's a sight for sore eyes. The company now earns 1.6% on its capital, because five years ago it was incurring losses. On top of that, what's interesting is that the amount of capital being employed has remained steady, so the business hasn't needed to put any additional money to work to generate these higher returns. With no noticeable increase in capital employed, it's worth knowing what the company plans on doing going forward in regards to reinvesting and growing the business. So if you're looking for high growth, you'll want to see a business's capital employed also increasing.

In another part of our analysis, we noticed that the company's ratio of current liabilities to total assets decreased to 43%, which broadly means the business is relying less on its suppliers or short-term creditors to fund its operations. Therefore we can rest assured that the growth in ROCE is a result of the business' fundamental improvements, rather than a cooking class featuring this company's books. Nevertheless, there are some potential risks the company is bearing with current liabilities that high, so just keep that in mind.

The Bottom Line

To bring it all together, Gemilang International has done well to increase the returns it's generating from its capital employed. Although the company may be facing some issues elsewhere since the stock has plunged 81% in the last five years. Regardless, we think the underlying fundamentals warrant this stock for further investigation.

Since virtually every company faces some risks, it's worth knowing what they are, and we've spotted 3 warning signs for Gemilang International (of which 2 are a bit unpleasant!) that you should know about.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

If you're looking to trade Gemilang International, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:6163

Gemilang International

An investment holding company, engages in the design, manufacture, and sale of bus bodies in Malaysia and Singapore.

Slight and slightly overvalued.

Market Insights

Community Narratives