- Hong Kong

- /

- Electrical

- /

- SEHK:505

Does Xingye Alloy Materials Group (HKG:505) Have A Healthy Balance Sheet?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Xingye Alloy Materials Group Limited (HKG:505) makes use of debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Xingye Alloy Materials Group

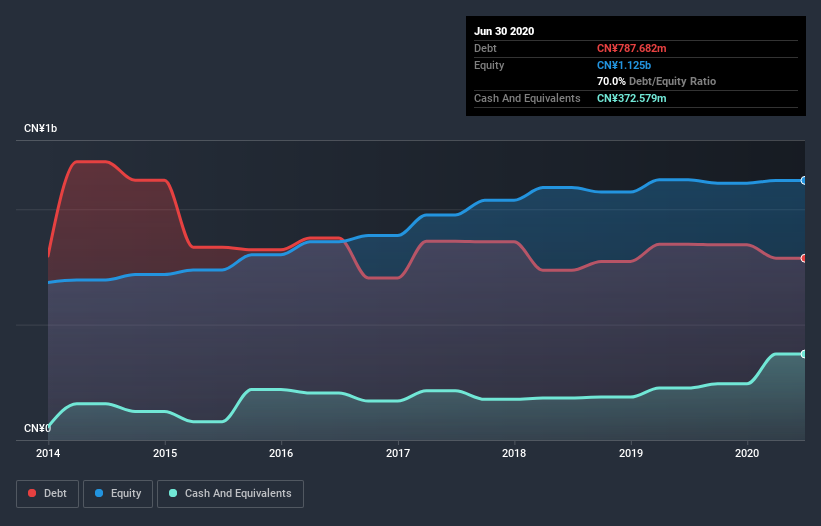

What Is Xingye Alloy Materials Group's Net Debt?

You can click the graphic below for the historical numbers, but it shows that Xingye Alloy Materials Group had CN¥787.7m of debt in June 2020, down from CN¥848.5m, one year before. On the flip side, it has CN¥372.6m in cash leading to net debt of about CN¥415.1m.

How Healthy Is Xingye Alloy Materials Group's Balance Sheet?

The latest balance sheet data shows that Xingye Alloy Materials Group had liabilities of CN¥1.39b due within a year, and liabilities of CN¥115.8m falling due after that. Offsetting these obligations, it had cash of CN¥372.6m as well as receivables valued at CN¥281.0m due within 12 months. So it has liabilities totalling CN¥853.4m more than its cash and near-term receivables, combined.

Given this deficit is actually higher than the company's market capitalization of CN¥731.4m, we think shareholders really should watch Xingye Alloy Materials Group's debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Xingye Alloy Materials Group has net debt worth 1.9 times EBITDA, which isn't too much, but its interest cover looks a bit on the low side, with EBIT at only 5.5 times the interest expense. While that doesn't worry us too much, it does suggest the interest payments are somewhat of a burden. Shareholders should be aware that Xingye Alloy Materials Group's EBIT was down 21% last year. If that earnings trend continues then paying off its debt will be about as easy as herding cats on to a roller coaster. There's no doubt that we learn most about debt from the balance sheet. But it is Xingye Alloy Materials Group's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Xingye Alloy Materials Group produced sturdy free cash flow equating to 74% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

Mulling over Xingye Alloy Materials Group's attempt at (not) growing its EBIT, we're certainly not enthusiastic. But at least it's pretty decent at converting EBIT to free cash flow; that's encouraging. Once we consider all the factors above, together, it seems to us that Xingye Alloy Materials Group's debt is making it a bit risky. That's not necessarily a bad thing, but we'd generally feel more comfortable with less leverage. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Consider for instance, the ever-present spectre of investment risk. We've identified 2 warning signs with Xingye Alloy Materials Group , and understanding them should be part of your investment process.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you decide to trade Xingye Alloy Materials Group, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

If you're looking to trade Xingye Alloy Materials Group, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About SEHK:505

Xingye Alloy Materials Group

Manufactures and trades in high precision copper plates and strips in Mainland China, South Korea, Taiwan, Hong Kong, Singapore, Bangladesh, Thailand, India, and internationally.

Solid track record with excellent balance sheet.

Market Insights

Community Narratives