Advertisement

- Hong Kong

- /

- Trade Distributors

- /

- SEHK:387

Leeport (Holdings) (HKG:387) Use Of Debt Could Be Considered Risky

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Leeport (Holdings) Limited (HKG:387) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Leeport (Holdings)

How Much Debt Does Leeport (Holdings) Carry?

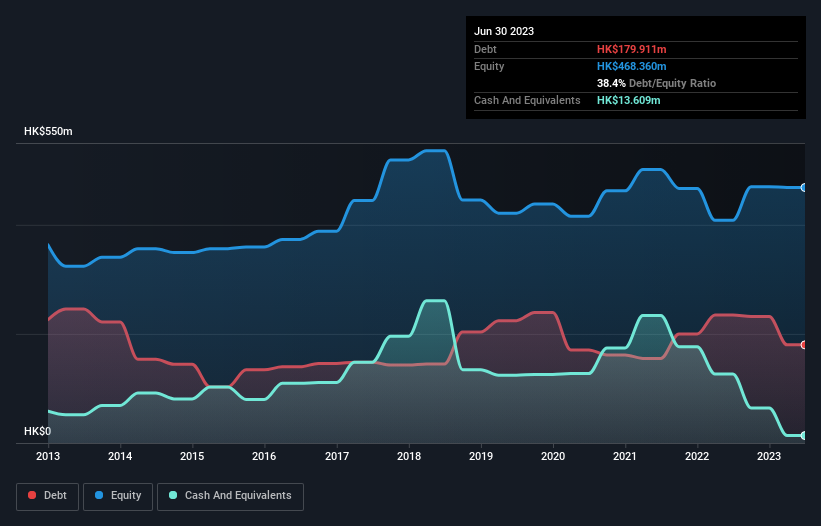

The image below, which you can click on for greater detail, shows that Leeport (Holdings) had debt of HK$179.9m at the end of June 2023, a reduction from HK$234.5m over a year. However, because it has a cash reserve of HK$13.6m, its net debt is less, at about HK$166.3m.

How Strong Is Leeport (Holdings)'s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Leeport (Holdings) had liabilities of HK$364.3m due within 12 months and liabilities of HK$30.3m due beyond that. On the other hand, it had cash of HK$13.6m and HK$240.7m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by HK$140.2m.

This deficit is considerable relative to its market capitalization of HK$140.3m, so it does suggest shareholders should keep an eye on Leeport (Holdings)'s use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Leeport (Holdings)'s debt is 4.1 times its EBITDA, and its EBIT cover its interest expense 3.5 times over. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. One redeeming factor for Leeport (Holdings) is that it turned last year's EBIT loss into a gain of HK$39m, over the last twelve months. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Leeport (Holdings)'s earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it's worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. During the last year, Leeport (Holdings) burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

Mulling over Leeport (Holdings)'s attempt at converting EBIT to free cash flow, we're certainly not enthusiastic. Having said that, its ability to grow its EBIT isn't such a worry. Overall, it seems to us that Leeport (Holdings)'s balance sheet is really quite a risk to the business. For this reason we're pretty cautious about the stock, and we think shareholders should keep a close eye on its liquidity. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 3 warning signs for Leeport (Holdings) (1 is a bit unpleasant!) that you should be aware of before investing here.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:387

Leeport (Holdings)

An investment holding company, engages in the trading of metalworking machinery, measuring instruments, cutting tools, and electronic equipment in the People’s Republic of China, Hong Kong, Singapore, Taiwan, Malaysia, and Indonesia.

Excellent balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|65.7% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|14.9% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|35.4% undervalued

DA

Community Contributor

Product Refresh And Global Expansion Will Empower Future Market Leadership

Fair Value US$202.60|21.0% undervalued

AN

Based on Analyst Price Targets