Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Royal Deluxe Holdings Limited (HKG:3789) makes use of debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Royal Deluxe Holdings

What Is Royal Deluxe Holdings's Net Debt?

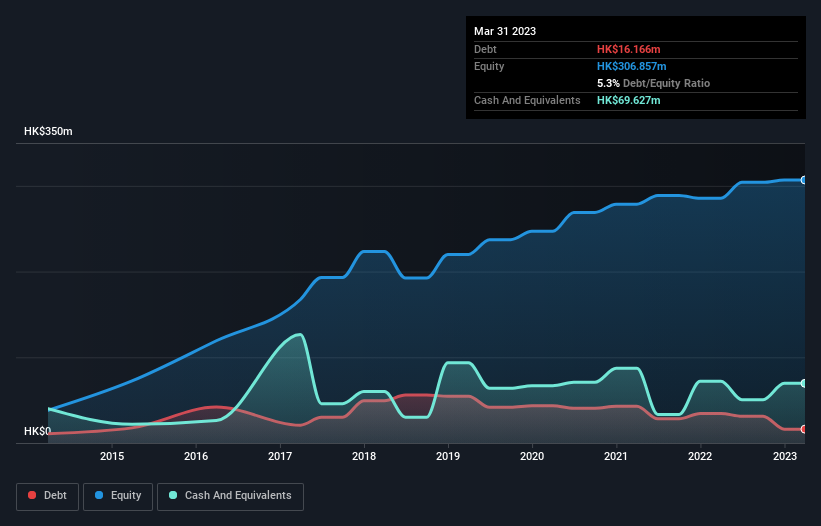

As you can see below, Royal Deluxe Holdings had HK$16.2m of debt at March 2023, down from HK$34.5m a year prior. However, it does have HK$69.6m in cash offsetting this, leading to net cash of HK$53.5m.

A Look At Royal Deluxe Holdings' Liabilities

We can see from the most recent balance sheet that Royal Deluxe Holdings had liabilities of HK$97.6m falling due within a year, and liabilities of HK$918.0k due beyond that. On the other hand, it had cash of HK$69.6m and HK$240.2m worth of receivables due within a year. So it actually has HK$211.3m more liquid assets than total liabilities.

This surplus liquidity suggests that Royal Deluxe Holdings' balance sheet could take a hit just as well as Homer Simpson's head can take a punch. On this view, lenders should feel as safe as the beloved of a black-belt karate master. Succinctly put, Royal Deluxe Holdings boasts net cash, so it's fair to say it does not have a heavy debt load!

Importantly, Royal Deluxe Holdings's EBIT fell a jaw-dropping 61% in the last twelve months. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. When analysing debt levels, the balance sheet is the obvious place to start. But it is Royal Deluxe Holdings's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Royal Deluxe Holdings has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Happily for any shareholders, Royal Deluxe Holdings actually produced more free cash flow than EBIT over the last two years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing Up

While it is always sensible to investigate a company's debt, in this case Royal Deluxe Holdings has HK$53.5m in net cash and a strong balance sheet. And it impressed us with free cash flow of HK$17m, being 243% of its EBIT. So we are not troubled with Royal Deluxe Holdings's debt use. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example Royal Deluxe Holdings has 3 warning signs (and 1 which can't be ignored) we think you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:3789

Royal Deluxe Holdings

An investment holding company, provides formwork erection and related ancillary services in Hong Kong.

Flawless balance sheet and good value.

Market Insights

Community Narratives