Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Royal Deluxe Holdings Limited (HKG:3789) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Royal Deluxe Holdings

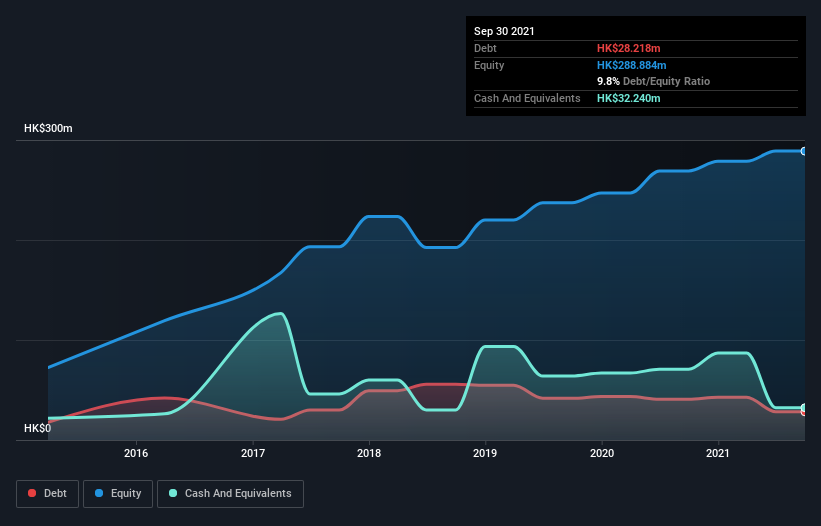

What Is Royal Deluxe Holdings's Debt?

As you can see below, Royal Deluxe Holdings had HK$28.2m of debt at September 2021, down from HK$40.6m a year prior. However, it does have HK$32.2m in cash offsetting this, leading to net cash of HK$4.02m.

How Healthy Is Royal Deluxe Holdings' Balance Sheet?

The latest balance sheet data shows that Royal Deluxe Holdings had liabilities of HK$109.1m due within a year, and liabilities of HK$162.0k falling due after that. Offsetting this, it had HK$32.2m in cash and HK$287.2m in receivables that were due within 12 months. So it actually has HK$210.2m more liquid assets than total liabilities.

This surplus strongly suggests that Royal Deluxe Holdings has a rock-solid balance sheet (and the debt is of no concern whatsoever). Having regard to this fact, we think its balance sheet is as strong as an ox. Succinctly put, Royal Deluxe Holdings boasts net cash, so it's fair to say it does not have a heavy debt load! There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Royal Deluxe Holdings will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Over 12 months, Royal Deluxe Holdings made a loss at the EBIT level, and saw its revenue drop to HK$684m, which is a fall of 18%. We would much prefer see growth.

So How Risky Is Royal Deluxe Holdings?

While Royal Deluxe Holdings lost money on an earnings before interest and tax (EBIT) level, it actually booked a paper profit of HK$20m. So when you consider it has net cash, along with the statutory profit, the stock probably isn't as risky as it might seem, at least in the short term. The next few years will be important as the business matures. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Royal Deluxe Holdings is showing 5 warning signs in our investment analysis , and 1 of those is concerning...

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:3789

Royal Deluxe Holdings

An investment holding company, provides formwork erection and related ancillary services in Hong Kong.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.8% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|43.5% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|61.4% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor