Advertisement

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. However, after briefly looking over the numbers, we don't think CITIC (HKG:267) has the makings of a multi-bagger going forward, but let's have a look at why that may be.

Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. To calculate this metric for CITIC, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

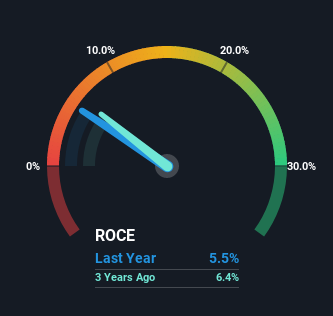

0.055 = HK$335b ÷ (HK$12t - HK$5.7t) (Based on the trailing twelve months to December 2022).

So, CITIC has an ROCE of 5.5%. On its own that's a low return, but compared to the average of 3.3% generated by the Industrials industry, it's much better.

View our latest analysis for CITIC

In the above chart we have measured CITIC's prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free report on analyst forecasts for the company.

SWOT Analysis for CITIC

Strength

- Earnings growth over the past year exceeded the industry.

- Net debt to equity ratio below 40%.

- Dividends are covered by earnings and cash flows.

Weakness

- Earnings growth over the past year is below its 5-year average.

- Interest payments on debt are not well covered.

- Dividend is low compared to the top 25% of dividend payers in the Industrials market.

Opportunity

- Annual earnings are forecast to grow for the next 3 years.

- Good value based on P/E ratio and estimated fair value.

Threat

- Debt is not well covered by operating cash flow.

- Annual earnings are forecast to grow slower than the Hong Kong market.

The Trend Of ROCE

There are better returns on capital out there than what we're seeing at CITIC. The company has consistently earned 5.5% for the last five years, and the capital employed within the business has risen 75% in that time. This poor ROCE doesn't inspire confidence right now, and with the increase in capital employed, it's evident that the business isn't deploying the funds into high return investments.

On a separate but related note, it's important to know that CITIC has a current liabilities to total assets ratio of 48%, which we'd consider pretty high. This effectively means that suppliers (or short-term creditors) are funding a large portion of the business, so just be aware that this can introduce some elements of risk. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

In Conclusion...

As we've seen above, CITIC's returns on capital haven't increased but it is reinvesting in the business. And investors may be recognizing these trends since the stock has only returned a total of 12% to shareholders over the last five years. So if you're looking for a multi-bagger, the underlying trends indicate you may have better chances elsewhere.

One more thing to note, we've identified 1 warning sign with CITIC and understanding it should be part of your investment process.

While CITIC isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:267

CITIC

Operates in the financial services, advanced intelligent manufacturing, advanced materials, consumption, and urbanization businesses in the Mainland of China, Hong Kong, Macau, Taiwan, and internationally.

Good value average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|4.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|32.5% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|21.9% undervalued

BL

Community Contributor