- Hong Kong

- /

- Trade Distributors

- /

- SEHK:223

We Think Shareholders Are Less Likely To Approve A Pay Rise For Elife Holdings Limited's (HKG:223) CEO For Now

Key Insights

- Elife Holdings to hold its Annual General Meeting on 29th of September

- CEO Sui Keung Chiu's total compensation includes salary of HK$1.20m

- The total compensation is similar to the average for the industry

- Over the past three years, Elife Holdings' EPS grew by 43% and over the past three years, the total loss to shareholders 66%

Shareholders of Elife Holdings Limited (HKG:223) will have been dismayed by the negative share price return over the last three years. Despite positive EPS growth in the past few years, the share price hasn't tracked the fundamental performance of the company. Shareholders may want to question the board on the future direction of the company at the upcoming AGM on 29th of September. They could also try to influence management and firm direction through voting on resolutions such as executive remuneration and other company matters. We think shareholders might be reluctant to increase compensation for the CEO at the moment, according to our analysis below.

Check out our latest analysis for Elife Holdings

Comparing Elife Holdings Limited's CEO Compensation With The Industry

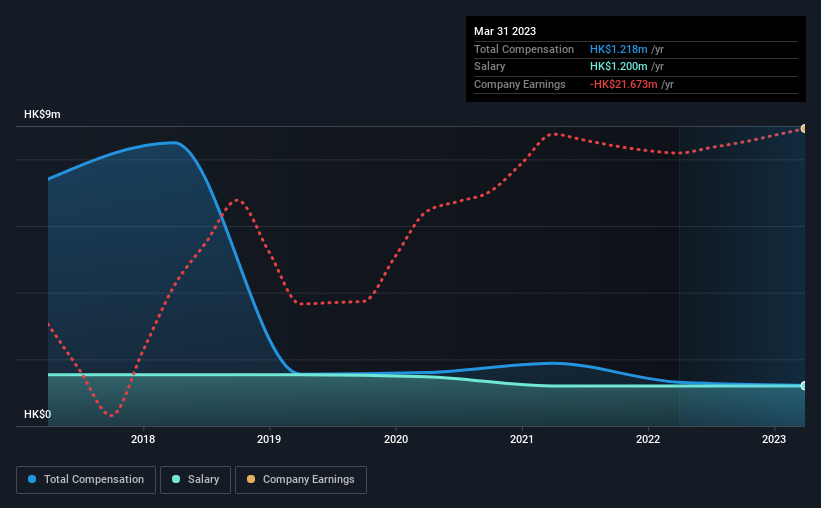

According to our data, Elife Holdings Limited has a market capitalization of HK$125m, and paid its CEO total annual compensation worth HK$1.2m over the year to March 2023. We note that's a small decrease of 7.2% on last year. Notably, the salary which is HK$1.20m, represents most of the total compensation being paid.

For comparison, other companies in the Hong Kong Trade Distributors industry with market capitalizations below HK$1.6b, reported a median total CEO compensation of HK$1.6m. From this we gather that Sui Keung Chiu is paid around the median for CEOs in the industry. What's more, Sui Keung Chiu holds HK$780k worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | HK$1.2m | HK$1.2m | 99% |

| Other | HK$18k | HK$112k | 1% |

| Total Compensation | HK$1.2m | HK$1.3m | 100% |

Speaking on an industry level, nearly 93% of total compensation represents salary, while the remainder of 7% is other remuneration. Elife Holdings pays a high salary, concentrating more on this aspect of compensation in comparison to non-salary pay. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Elife Holdings Limited's Growth Numbers

Elife Holdings Limited has seen its earnings per share (EPS) increase by 43% a year over the past three years. In the last year, its revenue is up 57%.

Shareholders would be glad to know that the company has improved itself over the last few years. The combination of strong revenue growth with medium-term EPS improvement certainly points to the kind of growth we like to see. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Elife Holdings Limited Been A Good Investment?

Few Elife Holdings Limited shareholders would feel satisfied with the return of -66% over three years. This suggests it would be unwise for the company to pay the CEO too generously.

In Summary...

Sui Keung receives almost all of their compensation through a salary. Despite the growth in its earnings, the share price decline in the past three years is certainly concerning. The stock's movement is disjointed with the company's earnings growth, which ideally should move in the same direction. Shareholders would be keen to know what's holding the stock back when earnings have grown. The upcoming AGM will be a chance for shareholders to question the board on key matters, such as CEO remuneration or any other issues they might have and revisit their investment thesis with regards to the company.

CEO pay is simply one of the many factors that need to be considered while examining business performance. That's why we did our research, and identified 4 warning signs for Elife Holdings (of which 1 is a bit unpleasant!) that you should know about in order to have a holistic understanding of the stock.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

If you're looking to trade Elife Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Elife Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:223

Elife Holdings

An investment holding company, engages in the supply chain business for branded goods and consumer products in Hong Kong and the People’s Republic of China.

Adequate balance sheet slight.

Market Insights

Community Narratives