Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Chanhigh Holdings Limited (HKG:2017) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out the opportunities and risks within the HK Construction industry.

What Is Chanhigh Holdings's Debt?

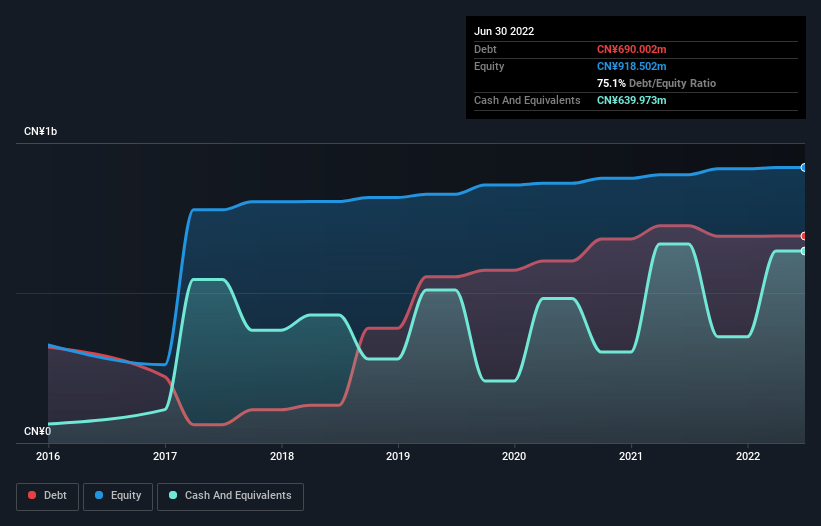

The image below, which you can click on for greater detail, shows that Chanhigh Holdings had debt of CN¥690.0m at the end of June 2022, a reduction from CN¥724.2m over a year. However, because it has a cash reserve of CN¥640.0m, its net debt is less, at about CN¥50.0m.

A Look At Chanhigh Holdings' Liabilities

The latest balance sheet data shows that Chanhigh Holdings had liabilities of CN¥1.23b due within a year, and liabilities of CN¥112.0m falling due after that. Offsetting these obligations, it had cash of CN¥640.0m as well as receivables valued at CN¥1.50b due within 12 months. So it can boast CN¥799.2m more liquid assets than total liabilities.

This luscious liquidity implies that Chanhigh Holdings' balance sheet is sturdy like a giant sequoia tree. With this in mind one could posit that its balance sheet means the company is able to handle some adversity.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While Chanhigh Holdings's low debt to EBITDA ratio of 0.92 suggests only modest use of debt, the fact that EBIT only covered the interest expense by 2.7 times last year does give us pause. So we'd recommend keeping a close eye on the impact financing costs are having on the business. Unfortunately, Chanhigh Holdings's EBIT flopped 18% over the last four quarters. If earnings continue to decline at that rate then handling the debt will be more difficult than taking three children under 5 to a fancy pants restaurant. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Chanhigh Holdings will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of that EBIT is backed by free cash flow. Considering the last three years, Chanhigh Holdings actually recorded a cash outflow, overall. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for an improvement.

Our View

When it comes to the balance sheet, the standout positive for Chanhigh Holdings was the fact that it seems able to handle its total liabilities confidently. However, our other observations weren't so heartening. To be specific, it seems about as good at (not) growing its EBIT as wet socks are at keeping your feet warm. When we consider all the factors mentioned above, we do feel a bit cautious about Chanhigh Holdings's use of debt. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 3 warning signs for Chanhigh Holdings (1 doesn't sit too well with us!) that you should be aware of before investing here.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2017

Chanhigh Holdings

An investment holding company, provides landscape and municipal works construction and maintenance services in the People’s Republic of China and Hong Kong.

Flawless balance sheet and good value.

Market Insights

Community Narratives