Advertisement

Beijing Jingcheng Machinery Electric Company Limited's (HKG:187) Shareholders Might Be Looking For Exit

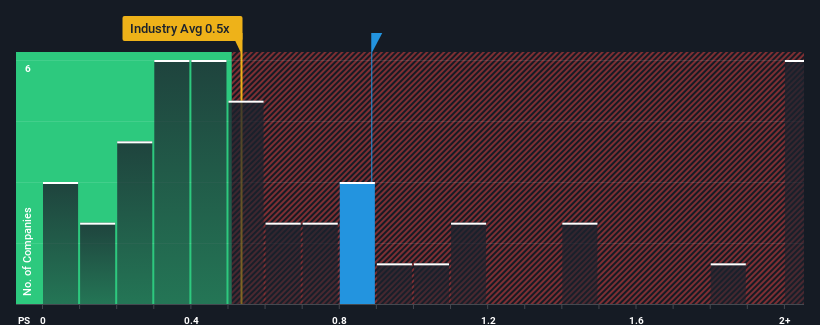

With a median price-to-sales (or "P/S") ratio of close to 0.5x in the Machinery industry in Hong Kong, you could be forgiven for feeling indifferent about Beijing Jingcheng Machinery Electric Company Limited's (HKG:187) P/S ratio of 0.9x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

View our latest analysis for Beijing Jingcheng Machinery Electric

How Beijing Jingcheng Machinery Electric Has Been Performing

For instance, Beijing Jingcheng Machinery Electric's receding revenue in recent times would have to be some food for thought. It might be that many expect the company to put the disappointing revenue performance behind them over the coming period, which has kept the P/S from falling. If you like the company, you'd at least be hoping this is the case so that you could potentially pick up some stock while it's not quite in favour.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Beijing Jingcheng Machinery Electric's earnings, revenue and cash flow.How Is Beijing Jingcheng Machinery Electric's Revenue Growth Trending?

In order to justify its P/S ratio, Beijing Jingcheng Machinery Electric would need to produce growth that's similar to the industry.

Retrospectively, the last year delivered a frustrating 1.4% decrease to the company's top line. Regardless, revenue has managed to lift by a handy 20% in aggregate from three years ago, thanks to the earlier period of growth. So we can start by confirming that the company has generally done a good job of growing revenue over that time, even though it had some hiccups along the way.

Comparing the recent medium-term revenue trends against the industry's one-year growth forecast of 12% shows it's noticeably less attractive.

With this information, we find it interesting that Beijing Jingcheng Machinery Electric is trading at a fairly similar P/S compared to the industry. Apparently many investors in the company are less bearish than recent times would indicate and aren't willing to let go of their stock right now. Maintaining these prices will be difficult to achieve as a continuation of recent revenue trends is likely to weigh down the shares eventually.

The Final Word

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Beijing Jingcheng Machinery Electric's average P/S is a bit surprising since its recent three-year growth is lower than the wider industry forecast. Right now we are uncomfortable with the P/S as this revenue performance isn't likely to support a more positive sentiment for long. Unless the recent medium-term conditions improve, it's hard to accept the current share price as fair value.

A lot of potential risks can sit within a company's balance sheet. Our free balance sheet analysis for Beijing Jingcheng Machinery Electric with six simple checks will allow you to discover any risks that could be an issue.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Beijing Jingcheng Machinery Electric might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:187

Beijing Jingcheng Machinery Electric

Manufactures and sells gas storage and transportation equipment in the People’s Republic of China and internationally.

Excellent balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|20.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.5% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|24.5% undervalued

CH

Community Contributor